Butterfly Options Strategy: Beginner's Guide

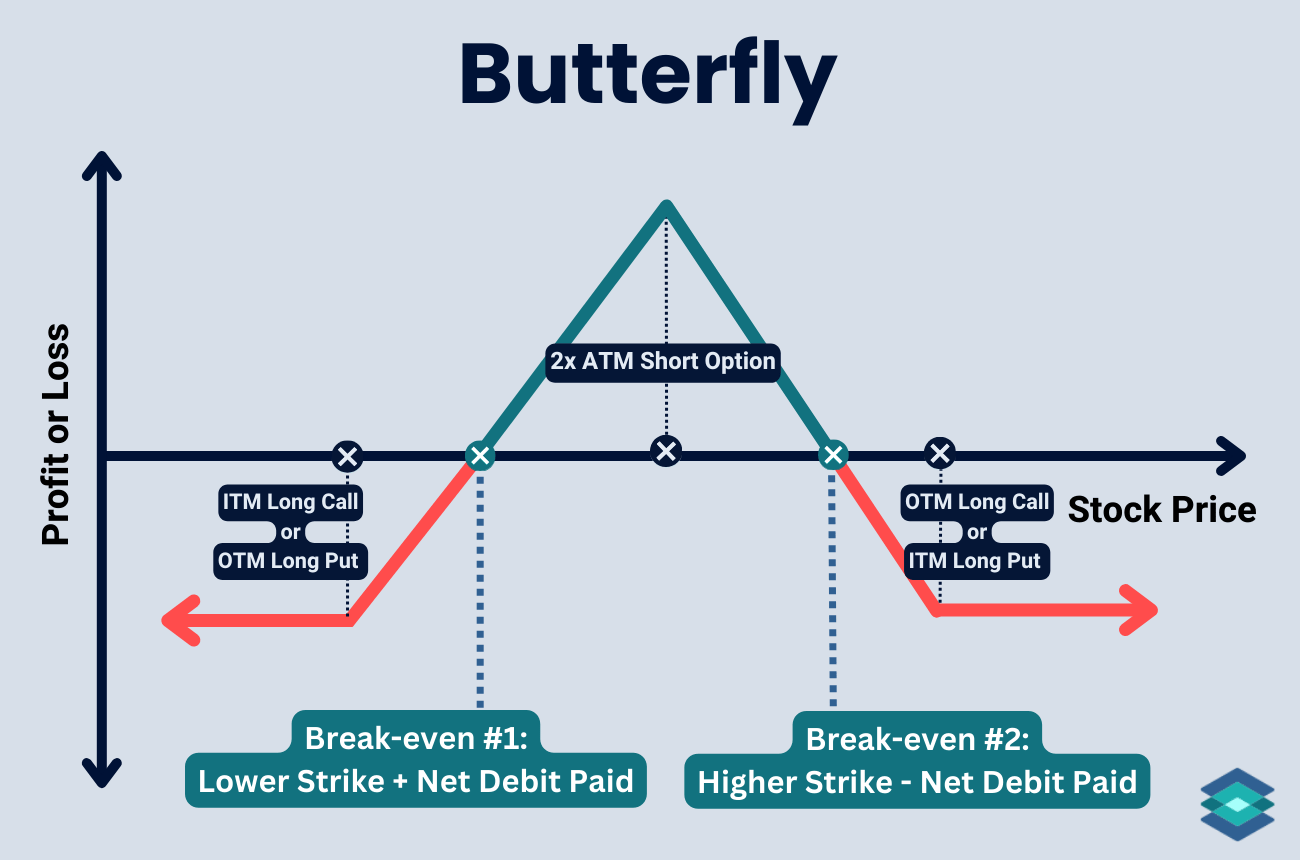

A long butterfly is a market-neutral, defined-risk options strategy using calls or puts: buy one lower strike, sell two middle strikes, and buy one upper strike.

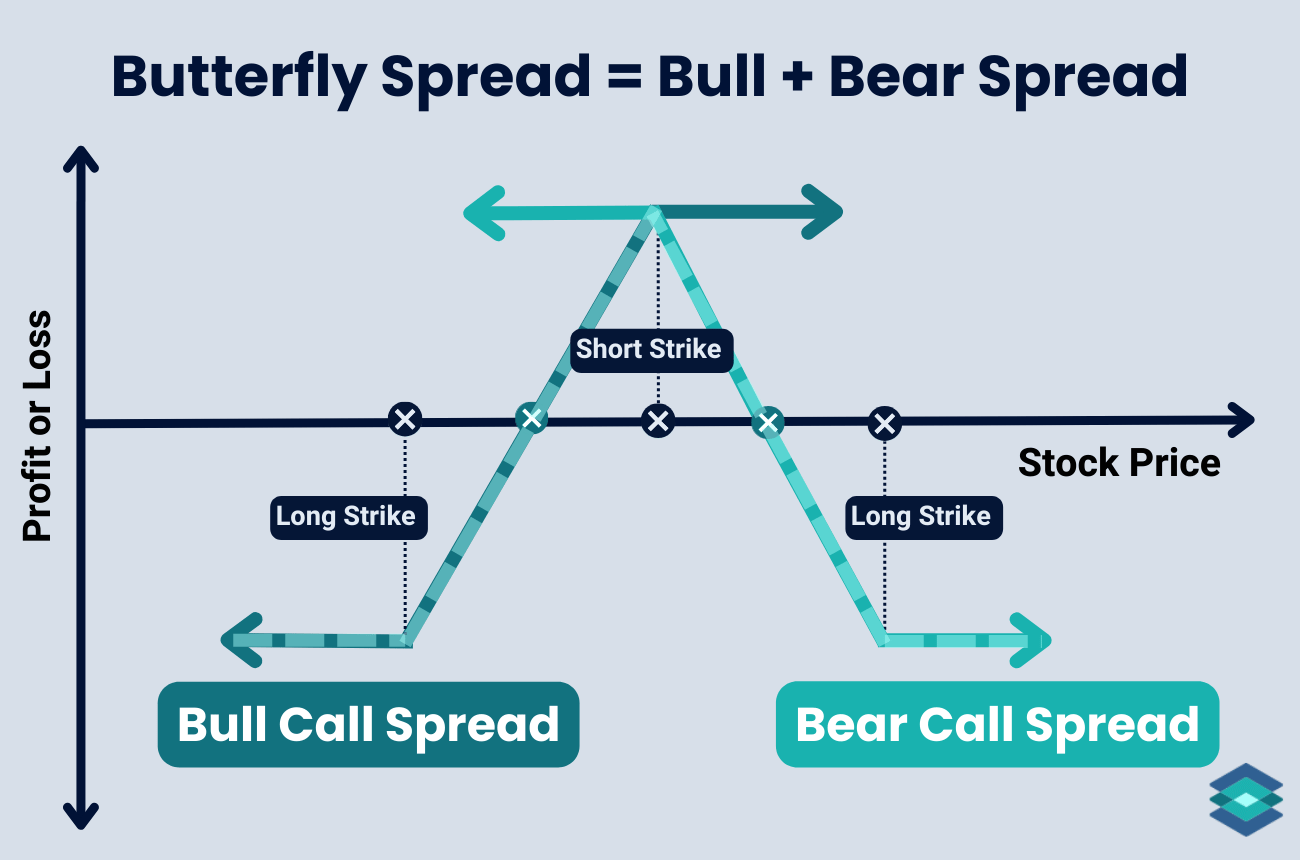

A long butterfly is built by combining two vertical spreads that share the same short strike and expiration cycle. The trade can be built by using all calls or all puts, but the outcomes are the same regardless.

Combined with a:

We can see the butterfly embedded in these two strategies by looking at the dashed lines below: the upward slope of the bull call spread and the downward slope of the bear call spread merge to form the butterfly payoff. This payoff would be identical if we had used puts.

It doesn’t make much of a difference whether you choose calls or puts - you just want the underlying to hug that middle, short strike price.

Butterflies can be traded long or short, but since most traders prefer the long version, we’ll refer to the long butterfly simply as ‘butterfly’ in this article.

Highlights

- Risk: Defined and capped at the net debit paid. Losses occur if the stock finishes outside the wings.

- Reward: Max profit is the spread width minus the debit, achieved only if the stock pins the body strike at expiration.

- Outlook: Market-neutral. Works best when the stock stays rangebound and implied volatility falls

- Edge: Low-cost way to bet on minimal movement, with limited risk and potential for outsized reward compared to cost.

- Time Decay: Favorable near the body. With both short strikes at the money, theta accelerates as expiration nears.

💡 Butterfly Strategy: Pro Takeaway

A butterfly is a net debit trade, yet it is market neutral. That may seem counterintuitive since most debit trades, like long calls or puts, only profit if the stock moves. You pay a debit because the in the money option costs more than the out of the money option on the other wing. The two short options in the middle reduce that cost but never erase it.

Even with a debit, the position is neutral because the deltas balance. The long in the money option carries a high positive delta, the long out of the money option carries a smaller positive delta, and the two shorts have negative delta, offsetting the long wings.

Think of it like buying a lottery ticket: you put up a small, known cost for the chance at a much larger payout if the stock finishes right at your middle strike.

Example:

- Stock trading at 100

- Buy 90 call, sell 2 × 100 calls, buy 110 call

- Net Debit = $1 ($100 total risk)

- Spread Width = 10 points

- Max Profit = 10 – 1 = $9 ($900) if stock pins 100 at expiration

- Max Loss = $1 ($100) if stock finishes outside the wings

That is risking $100 for a shot at $900, a 9 to 1 payoff. Most of the time, the stock will not land perfectly in the middle, but that is the trade-off: small, limited risk for the chance at an outsized reward.

The wider your wings, the more the trade behaves like a short straddle with a higher probability of profit. The tighter the wings, the cheaper the entry, but your payoff zone narrows.

In this article, we'll cover everything you need to know about the butterfly—when to use it, how to set it up, how to manage it, and some go-to tips for making it work.

Butterfly Trade Components

Here’s how you construct a long butterfly:

- Buy 1 option at the lower strike (if using calls) or at the higher strike (if using puts)

- Sell 2 options at the middle strike

- Buy 1 option at the higher strike (if using calls) or at the lower strike (if using puts)

- All options share the same expiration date

- The strikes are placed an equal distance apart

If your strikes are not equal distance, the trade is considered a broken wing butterfly, which has an entirely different payoff profile.

Ideally, butterflies are entered as one complete trade. If you leg in, you may expose yourself to directional risk.

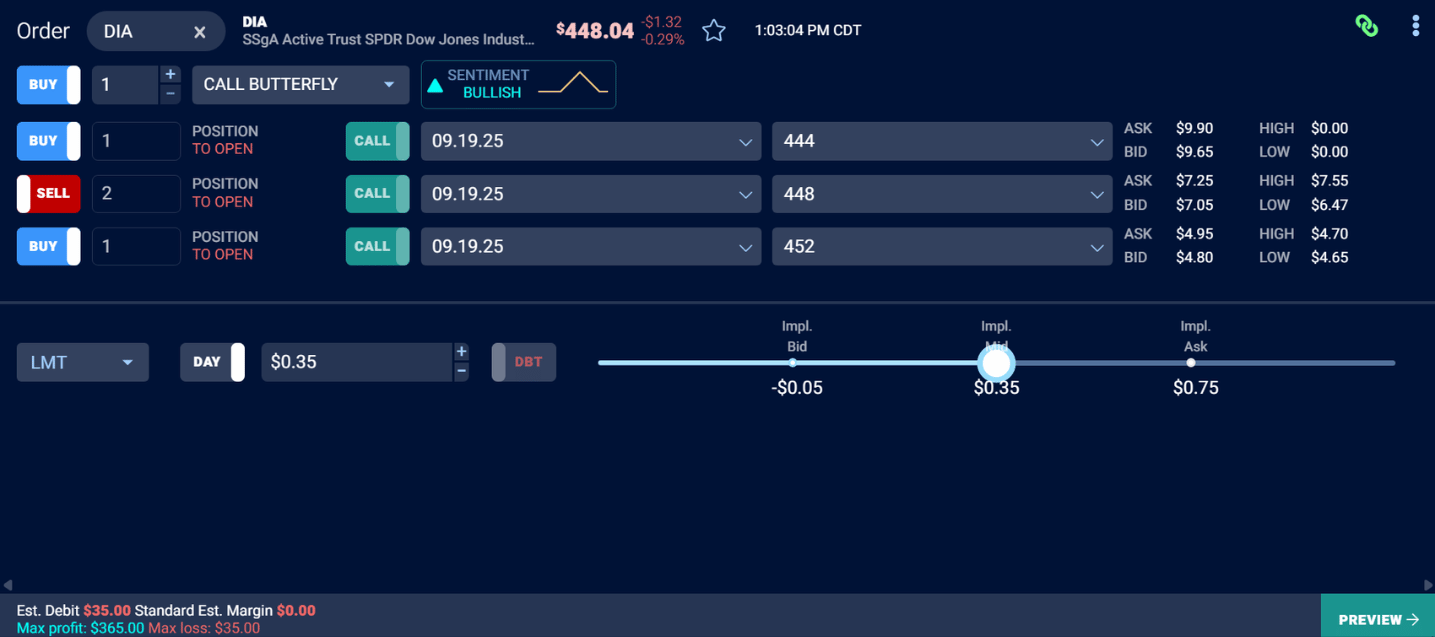

Here’s how you’d set up a short call butterfly on the TradingBlock dashboard:

Butterfly: Calls or Puts?

It doesn’t really matter if you build a butterfly with calls or puts. Calls usually have slightly better liquidity, but the difference is small unless you’re in an illiquid product.

If you’re holding through an ex-dividend date, avoid calls and use puts since they don’t carry dividend risk. That only applies to American-style options; index options like SPX or NDX are European-style, so they can’t be exercised early and don’t pay dividends.

If you have a bullish or bearish bias, you can place your butterfly’s body away from the money by shifting the center strike above or below the current price. But again, it doesn’t matter if you use calls or puts. The key is where you set that middle strike.

Butterfly Payoff Profile

Before moving to a real-world trade example, let’s examine the max profit, breakeven, and loss scenarios for a call butterfly spread on ABC.

Maximum Profit Zone

The max profit on a butterfly happens if the underlying asset closes right at the short strike at expiration. Here’s how you calculate max profit:

- Max Profit = (Spread Width – Net Debit)

For example, let’s say ABC is trading at $100 and we enter a butterfly:

- Buy the 95 call for $9.00

- Sell two 100 calls for $4.00 each

- Buy the 105 call for $1.00

That nets a total debit of $2.00 ($200). The spread width is $5 (100 – 95).

Therefore, the max profit is $5 – $2 = $3 ($300), realized if ABC finishes exactly at $100.

You can see the max profit zone below:

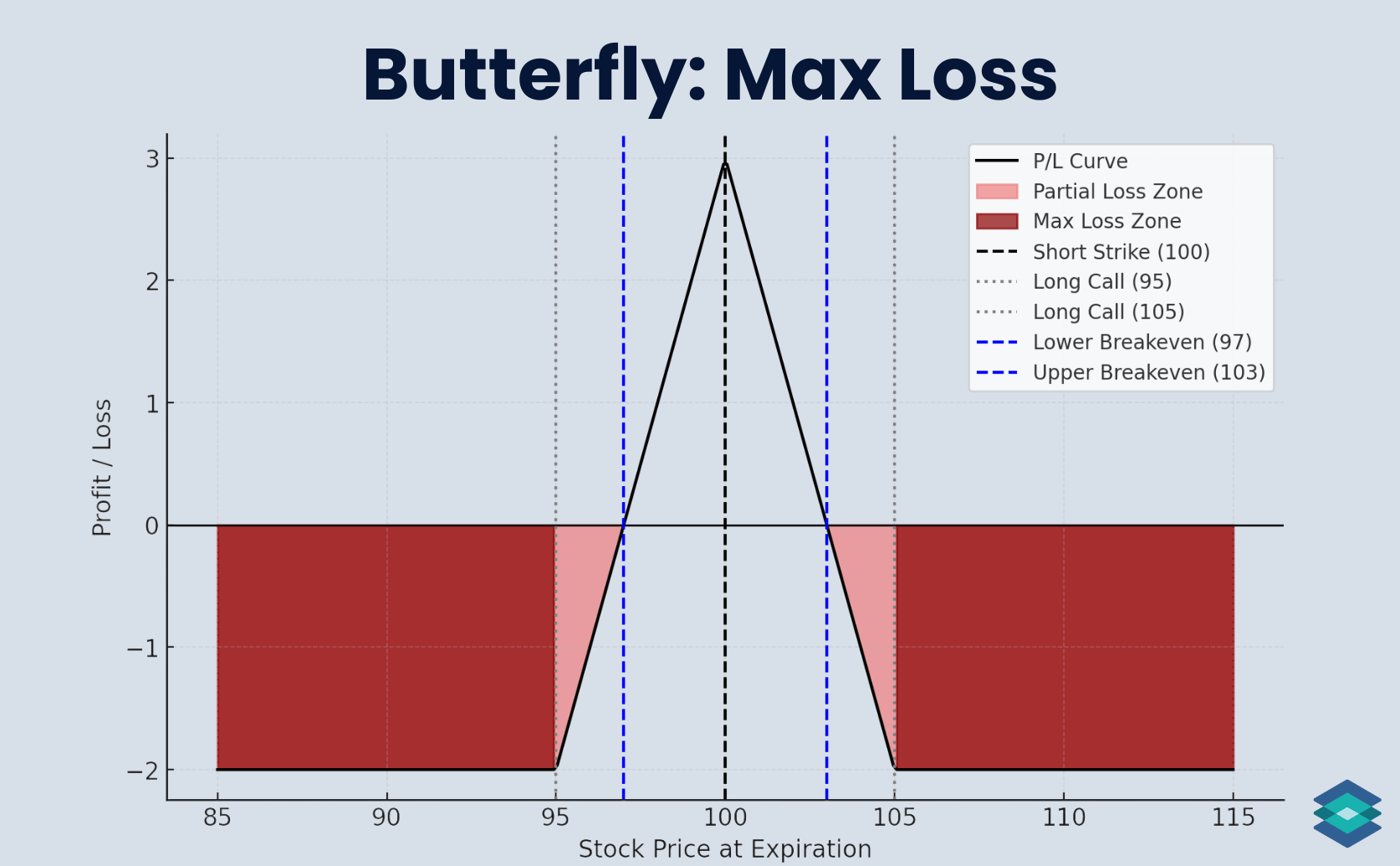

Maximum Loss Zone

The maximum you can lose on a butterfly is limited to the debit you pay to enter the trade. You always know this cost upfront.

- Max Loss = Net Debit Paid

For example, using our ABC butterfly:

- Buy the 95 call for $9.00

- Sell two 100 calls for $4.00 each

- Buy the 105 call for $1.00

That nets a total debit of $2.00 ($200) in option premium paid. This $200 is the most you can lose, no matter what happens (excluding commissions and slippage).

In our previous call butterfly trade, the max loss occurs if ABC closes at or below $95, or at or above $105 at expiration. In those cases, all the options either expire worthless or offset one another. Here’s how this works:

- At or below $95: all options expire worthless. The long 95 call has no value, the shorts aren’t challenged, and the long 105 call is also worthless. Your $200 debit is gone.

- At or above $105: the long 95 call is worth $10, the two short 100 calls lose $10 combined, and the 105 call is worthless at 105. The profits and losses offset, leaving the position with no value. Since you paid a $2 debit to enter, that debit is the max loss.

We can see this maximum loss zone below:

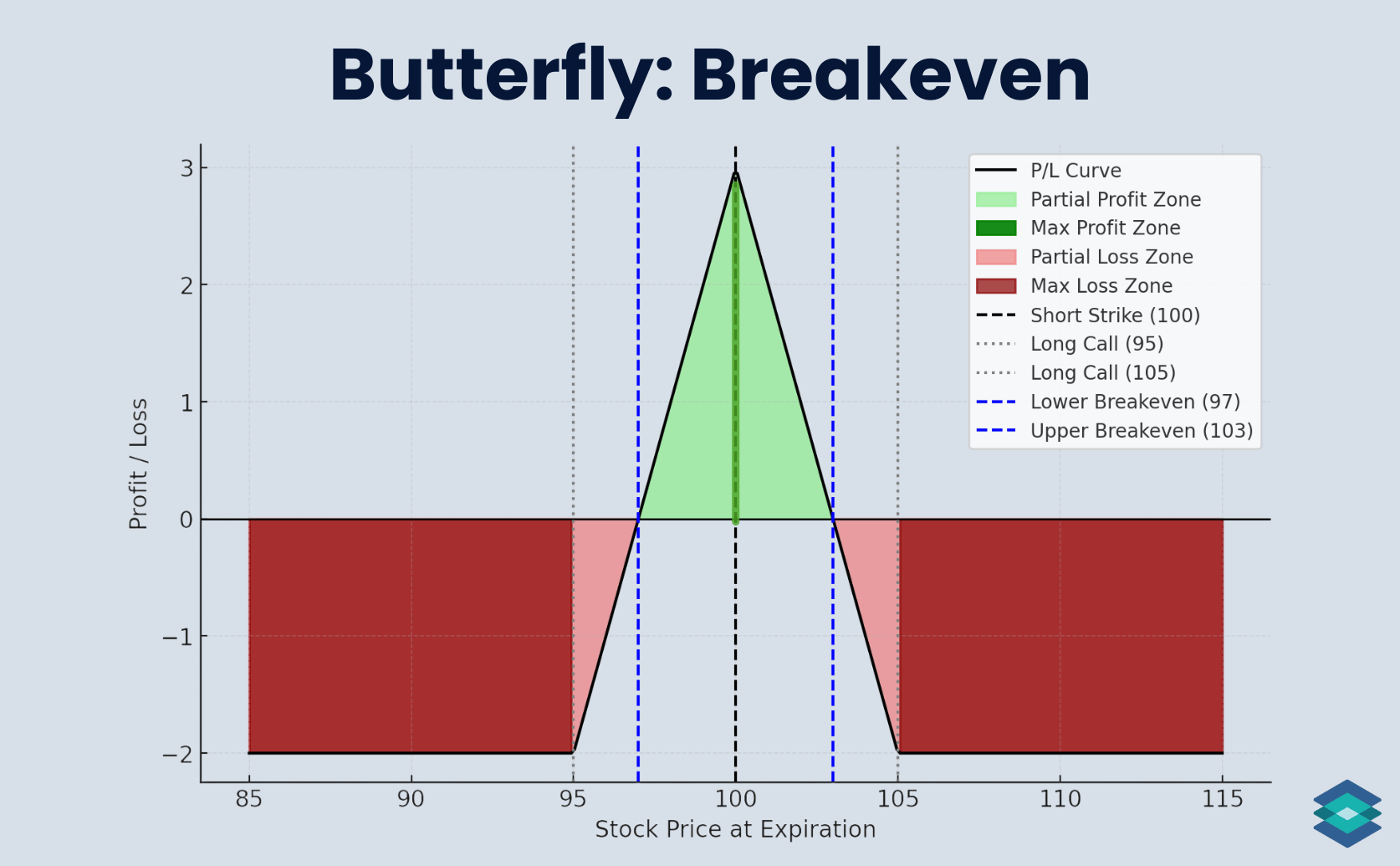

Breakeven Zone

A butterfly has two breakeven points. Here’s how you calculate them:

- Lower Breakeven = Lower Long Strike + Net Debit

- Upper Breakeven = Upper Long Strike – Net Debit

For our ABC trade:

- Buy the 95 call for $9.00

- Sell two 100 calls for $4.00 each

- Buy the 105 call for $1.00

That nets a debit of $2.00. Using the formulas:

- Lower breakeven = 95 + 2 = 97

- Upper breakeven = 105 – 2 = 103

If ABC finishes between $97 and $103 at expiration, the trade will make money. Profits build as the stock approaches the short strike of $100, with the peak profit realized right at that level.

We can see these breakeven zones below:

Butterfly Real World Trade Example

In this example, we’ll establish a long butterfly in DIA (Dow Jones ETF). Option premiums look more inflated than usual heading into earnings season, which makes the structure more attractive.

We’re using calls about four weeks from expiration, though the same setup could be built with puts. The goal is for DIA to hover near the short strike so the position benefits from time decay.

Let’s head to the options chain to find our strikes:

So we are going with a 4-point wide call butterfly in DIA, paying a net debit of $0.35 for the trade. Here’s how the pricing breaks down:

- Buy 1 × 444 call @ $9.78

- Sell 2 × 448 calls @ $7.15 each

- Buy 1 × 452 call @ $4.88

We are risking $35 per contract set to make up to $365 if DIA closes exactly at the short strike of 448. You can see why I called this trade a lottery ticket earlier.

Below is how the order appears as we send it off on the TradingBlock platform. When placing options trades, always start with the mid price. If you don't get filled immediately, incrementally increase the order by pennies or nickels until you do. Read more about options liquidity here.

DIA Butterfly Trade Details

And here are the details of the trade we just put on:

- Current DIA Price: $448.04

- Expiration: 29 days

- Buy 444 Call @ $9.78

- Sell 2 × 448 Calls @ $7.15 each

- Buy 452 Call @ $4.88

- Net Debit Paid: $0.35 ($35 total)

And here is the payoff profile:

- Lower Breakeven: 444 + 0.35 = $444.35

- Upper Breakeven: 452 – 0.35 = $451.65

- Max Profit: Width (4.00) – Debit (0.35) = $3.65 ($365 total)

- Max Loss: Debit paid = $0.35 ($35 total)

- Profit Range: $444.35 to $451.65

- Max Profit Zone: At $448 (the short strike) at expiration

- Risk/Reward: Risking $35 to make $365

Let’s now explore a couple of trade outcomes!

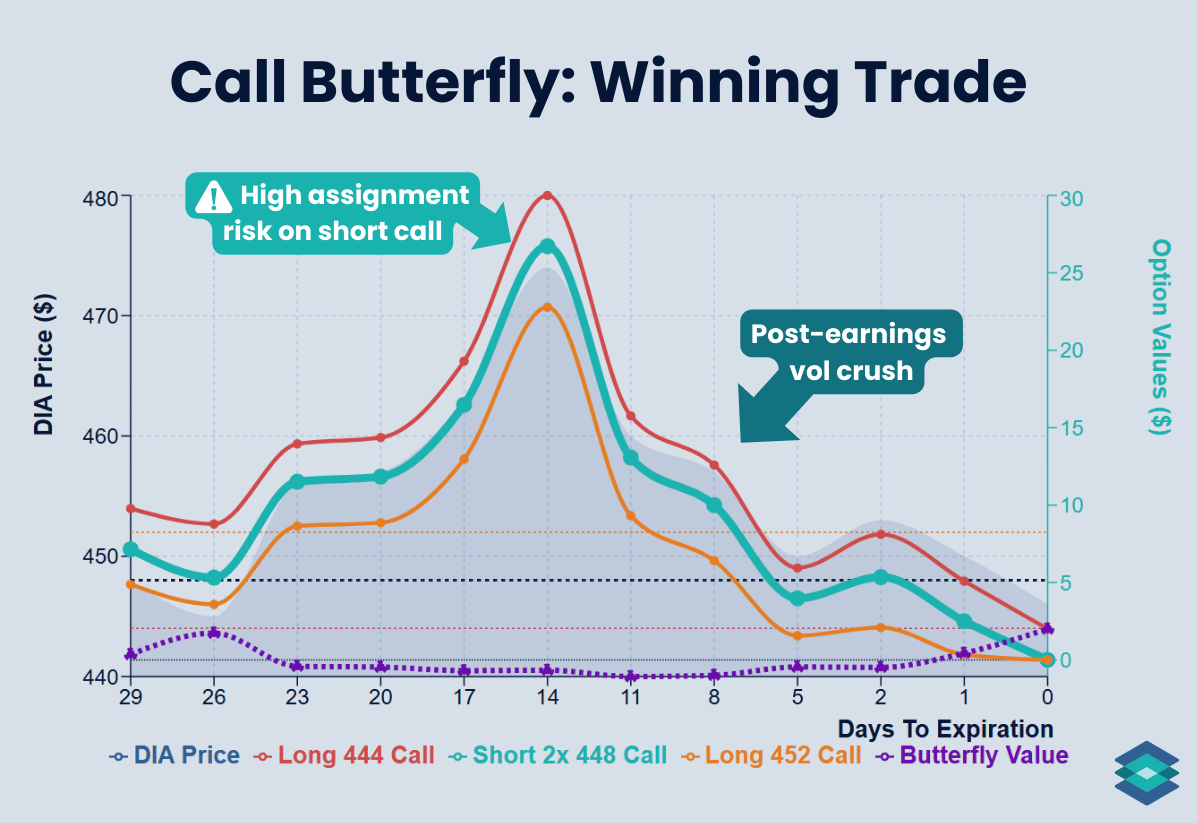

DIA Butterfly: Winning Trade

Twenty-nine days have passed, and our DIA options are set to expire. Earnings were in line (as anticipated), and the ETF closed at 446 on expiration day, just $2 below our entry. That trade worked out well for us!

Here’s where we ended:

- DIA Price: $448.04 → $446.00 ⬇️

- Expiration: 29 days → 0

- Buy 444 Call @ $9.78 → $2.00 (intrinsic)

- Sell 448 Call (x2) @ $7.15 → $0.00

- Buy 452 Call @ $4.88 → $0.00

- Final Value: Worth $2.00 at expiration

- Net Gain: $1.65 ($165 total)

- Percent of Max Profit Realized: ~45%

Although DIA slipped slightly, the butterfly structure still captured value because the close was within our breakevens. This highlights one of the butterfly’s strengths: you don’t need a perfect pin at the short strike to come out ahead.

Let’s now see how this trade played out in real-time.

DIA Winning Butterfly: Under the Hood

After earnings season, implied volatility collapsed, which gave the butterfly an immediate lift. Because butterflies are short vega, the drop in option premiums worked in our favor. From there, positive theta took over, steadily adding value as time passed.

You can see this in the purple butterfly line:

- The vol crush after earnings boosted the position right away.

- As DIA hovered closer to the 448 short strike, the payoff “tent” filled out and the butterfly’s value rose further.

- Even though DIA finished at 446 instead of pinning 448 exactly, the trade still closed well inside the breakevens and locked in a solid gain.

DIA Butterfly: Losing Trade

Twenty-nine days have passed, and our DIA options are set to expire. After a brief rally, DIA sold off sharply and closed at $425 on expiration day, far below our profit range. This outcome left our butterfly worthless at expiration.

Here’s where we ended:

- DIA Price: $448.04 → $425.00 ⬇️

- Expiration: 29 days → 0

- Buy 444 Call @ $9.78 → $0.00

- Sell 448 Call (x2) @ $7.15 → $0.00

- Buy 452 Call @ $4.88 → $0.00

- Final Value: Worth $0.00 at expiration

- Net Loss: $0.35 ($35 total)

- Percent of Max Loss Realized: 100%

Because DIA finished well outside of the breakevens, none of the butterfly’s options held any value at expiration. This highlights the defined-risk nature of the trade: while the loss was the maximum possible, it was capped at the original debit paid.

We paid only $0.35 for this butterfly to make up to $3.65. You don’t need to be a math scholar to see the odds aren’t stacked in your favor!

DIA Losing Butterfly: Under the Hood

In this outcome, DIA first rallied hard and then sold off sharply. On the way down, it crossed our 448 short call strike with about 8 days to expiration.

At that point, we could have exited the spread for around $0.78. Since we paid only $0.35 to enter, that would have locked in a 123% return. Not bad, considering how the trade ultimately finished worthless.

As the saying on Wall Street goes: bulls make money, bears make money, but pigs get slaughtered.

Butterfly Margin Requirements

The long butterfly is a defined-risk debit trade, so margin requirements are simple. You only need to post the net debit you pay to enter the position, plus commissions and fees.

- Margin Requirement = Net Debit Paid

Because the risk is capped at the debit, brokers don’t require additional margin. This makes the long butterfly one of the most capital-efficient multi-leg strategies: you know your maximum loss the moment you put the trade on.

Choosing Your Delta and Strikes

In options trading, delta is the option Greek that refers to how much an option's value may change given a $1 move up or down in the underlying asset. Delta also tells us:

- The number of shares an option ‘trades like’

- The probability an option has of expiring in the money

Assuming you are buying an at the money butterfly, which is how most traders structure it, the short strike options each have a delta of about -0.50. Since you are short two of those calls, the combined delta is –1.00 delta.

But the butterfly is a delta-neutral trade. That means the long options, or wings, must carry positive delta to offset the negative delta from the two shorts.

The sum of these deltas must equal, or at least come very close to, zero depending on the exact moneyness of the at the money option.

We can see this for a 15-point call butterfly on SPX (Standard & Poor’s 500 Index) below:

The long 0.57 delta and long 0.46 delta together offset the two short 0.52 deltas. The result is a net delta of about –0.01, which is effectively neutral at entry.

Wide vs. Tight Wings

When you buy a butterfly, you choose how far out to place the long wings.

- Wider wings cost more but give the trade a larger profit zone and higher potential max profit.

- Tighter wings are cheaper but concentrate risk and reward in a narrower range around the short strike.

Remember, one of your wings is in the money. The deeper in the money it is, the more expensive it becomes, and you will be paying more for this than what you save on the out of the money wing.

Theta (Time Decay) in Butterflies

Butterflies profit when the underlying asset stays close to the short strike and time passes. As time passes, and price and implied volatility remain the same, both the long and short options lose value.

However, the structure has two short options at the body against one long option on each wing. This creates a net positive theta effect. In other words, the decay of the short options outweighs the net decay of the longs, so time decay benefits the butterfly as time passes.

At expiration, if the underlying asset is trading at the short strike price:

- Short options (body): expire worthless at the pin, or are offset by the long wings if price moves away.

- In the money long wing: holds intrinsic value and defines the maximum profit outcome.

- Out of the money long wing: expires worthless if price stays near the body, but acts as protection if the underlying moves beyond the spread.

We can see how the passage of time benefits the trade below:

Butterflies and Implied Volatility

A long butterfly is a short volatility trade. It benefits if implied volatility (IV) falls after you put it on. That’s why traders usually enter when IV is relatively high and likely to decline.

So how do you measure whether IV is “high” or “low”? Two common tools are:

- IV Rank – compares today’s IV to its range over the past year. (If IV has ranged from 15% to 45% in the past year and is now at 40%, IV Rank is near the top of that range.)

- IV Percentile – shows how often IV has been lower than the current level in the past year.

Both are useful, but IV Rank is the go-to for quick comparisons across different underlyings.

- High IV entry (better): When IV Rank is above 30–40%, the short body options are richly priced compared to the wings. This reduces your net debit and sets you up to benefit if volatility contracts.

- Low IV entry (riskier): When IV Rank is below 20%, the body is relatively cheap. That means you pay more for the structure and are exposed if volatility expands, since the butterfly can quickly become more expensive to close.

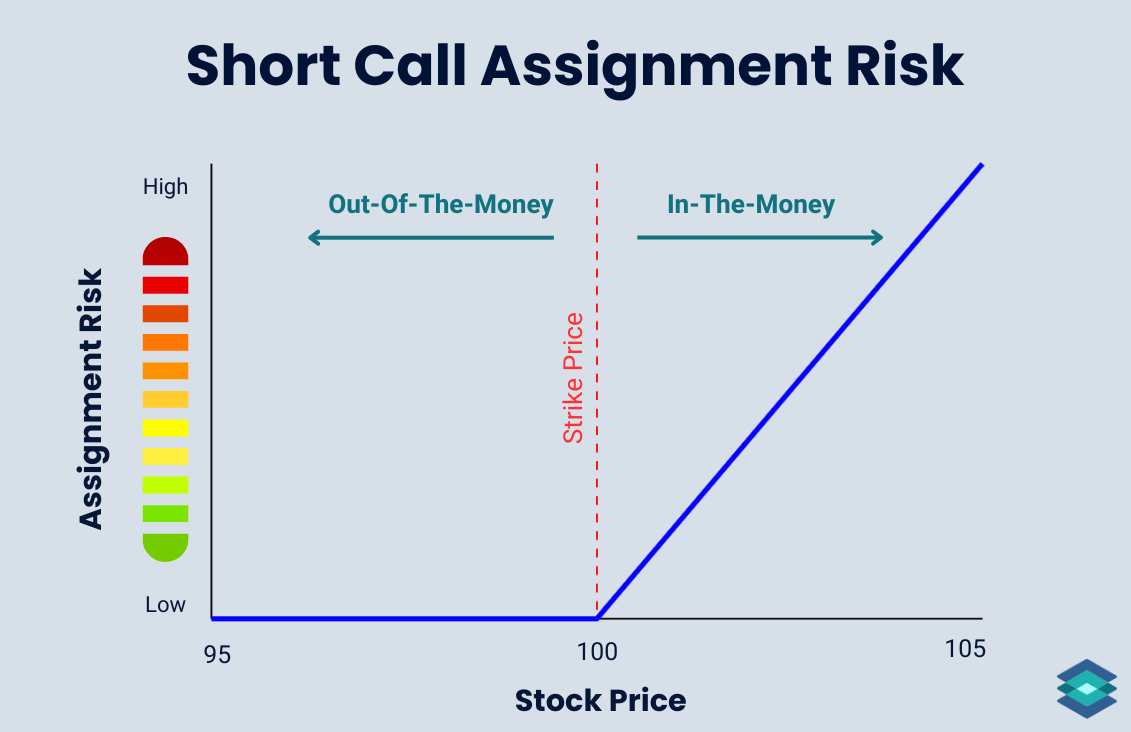

Managing Assignment Risk

If you are trading butterflies in American-style options, such as stocks and ETFs, the short legs are exposed to assignment risk. Since the shorts are placed at the money, there is always a chance of early assignment. That risk increases as time passes and the options move deeper in the money.

If you do get assigned on your two short options, you have a few ways to manage the trade:

- Accept the assignment: Hold the resulting stock position and manage it directly, though this exposes you to directional risk.

- Exercise your in the money long option: Use the ITM long to offset part of the assignment. Since you’re short two options and likely only long one in the money at this point, exercising will only cover half the stock exposure. Out of the money longs should not be exercised because they have no intrinsic value.

- Close the entire position in the market: Exit both the stock created by assignment and any remaining option legs to flatten out completely.

Butterflies and The Greeks

In options trading, the Greeks are a set of risk metrics that help estimate how an option’s price will respond to changes in key market variables. Here are the five most important Greeks to know:

- Delta – shows how much the option price changes for a $1 move in the stock.

- Gamma – shows how much delta shifts when the stock moves $1.

- Theta – shows how much the option loses in value each day from time decay.

- Vega – shows how much the option price changes for a 1% change in implied volatility.

- Rho – shows how much the option price changes for a 1% change in interest rates.

And here is the relationship between butterflies and these Greeks:

⚠️ Long butterflies are advanced option strategies. Risk is capped at the debit paid, but sharp moves away from the body strike often result in a full loss of that debit. This strategy is not suitable for all investors. Outcomes can also be affected by assignment risk, commissions, fees, and slippage—factors not reflected in the examples. Always read The Characteristics and Risks of Standardized Options before trading.

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

FAQ

A butterfly can be a good strategy if your market outlook is neutral. It’s designed to profit when the underlying stays near a specific price level. Because risk is capped at the debit paid, it offers defined risk with a potentially attractive reward. However, the stock must finish within a relatively narrow range for maximum profit, so it’s not suited for every situation.

If a stock is trading at $100, you could buy the 95 call, sell two 100 calls, and buy the 105 call. This long call butterfly might cost a $2 debit, which is also the maximum risk. The maximum profit is $3 if the stock finishes exactly at $100 at expiration, since the 95–100 spread is worth $5 minus the $2 debit. The breakeven points are $97 on the downside and $103 on the upside.

A butterfly has two breakeven points. They are calculated as:

- Lower Breakeven = Lower Long Strike + Net Debit

- Upper Breakeven = Upper Long Strike – Net Debit

When volatility is high and expected to fall, short volatility trades are favored. Credit spreads and iron condors fit that mold, but butterflies do too. Even though a butterfly is entered for a debit, high implied volatility makes the short body options expensive compared to the wings, lowering the net cost. If volatility contracts after entry, the butterfly gains value.

Traders usually buy butterflies when they expect the underlying to remain near a certain price into expiration. They are often used around earnings or major announcements when implied volatility is high but the trader believes the stock will not move as much as the options market is pricing in.

A butterfly spread uses either all calls or all puts with three strikes, while an iron butterfly combines both calls and puts by selling a straddle at one strike and buying protective wings above and below.

Maximum profit happens when the stock finishes exactly at the short strike at expiration, allowing you to keep the entire premium collected.