Short Strangle Options Strategy: Beginner's Guide

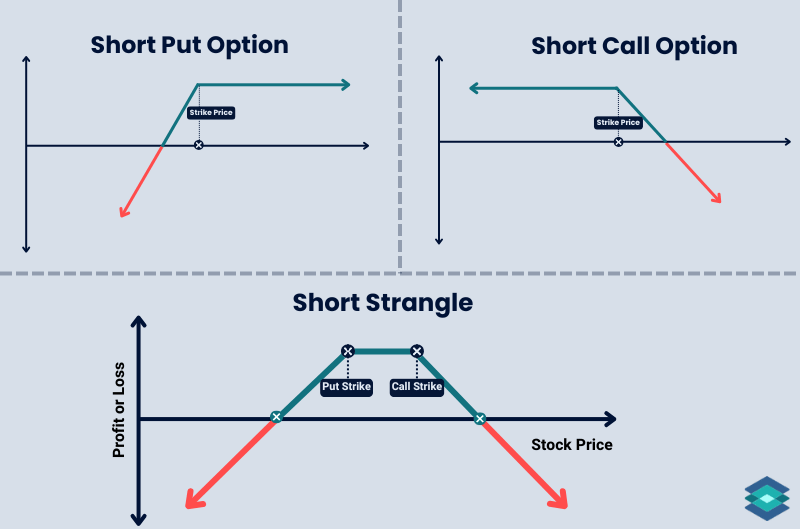

The short strangle options trade consists of selling an out of the money call and put option with the same expiration date. It is a net credit trade with infinite loss potential on the call side and substantial downside risk on the put side.

.png)

The short strangle is best suited for investors expecting volatility to fall and the underlying price to remain between the strikes sold by option expiration. It’s a high-risk trade, but considered less risky than its cousin, the short straddle, because the options sold are further out of the money, reducing some exposure. Like all net short option trades, the short strangle profits from time decay and a fall in implied volatility.

Highlights

- Risk: Unlimited on the call side; substantial on the put side. One big move can wreck the trade.

- Reward: Max profit is the credit received, realized if the stock stays between strikes at expiration.

- Outlook: Neutral to slightly directional, works best when the stock stays rangebound and IV drops.

- Edge: Short strangles offer wide breakevens and benefit from inflated option premiums.

- Time Decay: Strongly favorable: theta ramps up as expiration approaches.

- 1 Standard Deviation: Preferred SD for most traders, strikes are typically set around the 16 delta mark on both sides.

- Approximate Profitability: Around 68% probability of profit with 1 SD.

💡 Short Strangle Strategy: Pro Takeaway

The short strangle is a net credit, high-probability options trading strategy with considerable risk. The trade involves selling an out of the money call and an out of the money put, both with the same expiration date.

This contrasts the straddle, which involves selling a call and put option at the same strike price.

It's called a strangle because your strike prices are spread apart, kind of "strangling" the stock between them. In contrast, you can think of the straddle as standing over and "straddling" the strike price.

Both strategies bet on the stock staying put, but the strangle gives you a little more breathing room and, consequently, less profit potential as it takes in less option premium.

Strangles have lower P/L swings and volatility exposure than straddles because they involve selling out of the money options, which have lower delta and gamma.

In this article, we'll cover everything you need to know about the short strangle—when to use it, how to set it up, how to manage it, and some go-to tips for making it work.

🤔 New to options? It helps immensely to understand both the short put and short call strategies before jumping into strangles.

Short Strangle Trade Components

Here’s how you build a short strangle:

- Sell 1 out of the money call

- Sell 1 out of the money put

- Same expiration date for both

This sets up a net credit trade with no directional bias, but more room to be wrong than a straddle. You’re collecting premium on both sides, betting the stock stays between the strikes through expiration.

Ideally, strangles are placed as one order. If you leg in, you’re exposed to directional risk.

Here’s how to set it up on the TradingBlock dashboard:

Market Outlook: When to Sell a Strangle

Here are a few scenarios where it may make sense to sell a strangle:

- Neutral to Mild Directional Bias: You’re expecting the stock to stay within a range

- High Implied Volatility: Elevated IV means fatter premiums. Sell the strangle when IV is high, but only if you think it’ll drop before expiration.

- You’re Ready to Manage: One or even both sides of your trade may approach being in the money over the trade duration. Be prepared to roll, hedge, or adjust the trade if the stock drifts too close to either strike.

- You Understand Assignment Risk: If you’re trading American-style options, assignment risk ramps up the deeper your option goes in the money and the closer you get to expiration.

Short Strangle Payoff Profile

Let’s break down max profit, breakevens, and max loss.

Maximum Profit Zone

Max profit on a short strangle is:

Max Profit = Total Credit Received

If the stock stays between your short strikes, you collect the full premium on option expiration.

Let’s take a look at an example of a short strangle on ABC where the stock is currently trading at $100/share:

- Sell 105 call for $2.50

- Sell 95 put for $2.50

- Total credit: $5.00 ($500 max profit)

- Max profit zone: 95 to 105

You keep the $500 if the stock finishes anywhere in that 10-point window, as seen below:

Breakeven Zone

A short strangle has two breakeven points: one on the upside, one on the downside. Here’s how to find them:

Upper Breakeven = Call Strike + Total Credit Received

Lower Breakeven = Put Strike – Total Credit Received

Using our previous example:

We sold the 95 put and the 105 call on ABC for a combined credit of $5.00.

So:

- Lower breakeven = 95 – 5 = 90

- Upper breakeven = 105 + 5 = 110

Maximum Loss Zone

The short strangle carries real risk on both sides, and it’s not capped. Here’s where the risk is:

Max loss (call side) = ∞

Max loss (put side) = Strike Price – Credit Received

Using our example:

- Sold 95 put and 105 call

- Total credit: $5.00

- Put side max loss = 95 – 5 = $90/share

- Call side max loss = unlimited

Short Strangle Margin Requirements

With a short strangle, the stock can finish above one strike price or below the other, but not both. Therefore, it doesn’t make sense for brokers to charge full margin on the call and the put.

Most brokers base margin on the riskier leg, then add the credit from the other side.

For example, let’s say you sell the 95 put and 105 call on ABC for a total credit of $5.00. Here's how that might look:

- Short 95 put = $2.75 credit → $3,000 margin

- Short 105 call = $2.25 credit → $2,500 margin

Your broker may use the put as a basis since the margin for this leg is higher. Then they may add in the call credit:

$3,000 + $225 = $3,225 total margin requirement

Different brokers use different margin engines, so the requirements for naked trades like the short strangle can vary greatly.

Skewing the Strangle

So far we’ve only covered the neutral strangle, which involves selling a put and a call the same distance away from the stock price.

But what if you have some directional bias? That’s where skew comes in. You can skew your strangle to account for different market forecasts.

The image below shows how you can set up a neutral, bullish, or bearish strangle with the underlying trading at $100.

If you skew your strangle too far, you might sell options at or even in the money. One risk here is that in the money options don’t decay as fast as out of the money options, so be careful how far you tilt the trade or it may not resemble a strangle at all.

Other risks of skewing strangles include:

- Reduces your probability of profit

- Increases buying power requirements

- Exposes you to greater directional risk

- Increase assignment risk

Short Strangle: IBIT Trade Example

The market’s been incredibly volatile over the past few weeks. With inflation jitters and the ballooning budget deficit, bitcoin’s been having huge swings. Implied volatility is through the roof, which means premiums are ramped up, and as a seller of options, I love that.

I think the volatility will settle over the next five weeks or so, so I will sell a strangle on IBIT (iShares Bitcoin Trust).

If I believed IBIT would stay completely flat, I’d sell an at the money straddle. But my conviction isn’t absolute, so I’m giving myself some breathing room and going with a short strangle instead (neutral strangle).

Here’s why I’m choosing IBIT:

- 1x1 tracking on bitcoin spot

- Tight bid/ask spreads and solid options volume

- Plenty of strikes and expirations to work with

Let’s head over to the TradingBlock dashboard to locate the IBIT options chain and find an expiration and strike price that works for us:

IBIT Trade Setup

IBIT is trading around $60, and we’re selling the 65 calls and 55 puts, both about 8% out of the money. That gives us some cushion on both sides while still collecting a solid credit thanks to the elevated IV.

Here’s how the trade setup looks on TradingBlock:

Note that it’s important ALWAYS to use limit orders when trading options. It’s also a good idea to start at the midpoint and work your way down (or up) in penny/nickel increments until you get a fill you like.

We’re going to assume we got filled at 2.84, the mid.

IBIT Trade Details

- Underlying: IBIT trading at $59.64

- Expiration: 37 days (July 11, 2025)

- Sell 65 Call @ $1.53 (mid)

- Sell 55 Put @ $1.31 (mid)

- Net Credit Received: $2.84 ($284 total)

- Breakeven Prices:

- Lower Breakeven = 55 – 2.84 = 52.16

- Upper Breakeven = 65 + 2.84 = 67.84

- Max Profit: $2.84 or $284 (if IBIT stays between strikes)

- Max Loss: Unlimited on the upside / Substantial on downside

- Estimated Margin Requirement: $595

Bear in mind the high margin requirement for this trade. With the risk-free rate currently over 4%, don't forget to factor in that opportunity cost when making your trade.

Let’s now explore a few different outcomes!

IBIT: Winning Trade Outcome

37 days have passed, and expiration is upon us. Let’s see how our trade performed:

- IBIT Price: $59.64 → $57.00 ⬇️

- Expiration: 37 days → 0

- Sell 65 Call @ $1.53 → $0.00

- Sell 55 Put @ $1.31 → $0.00

- Final Value: $0.00 closed at full profit

- Net Profit: $2.84 – $0.00 = $2.84 ($284 total)

- Percent of Max Profit: 100% ✅

Now, on paper, this looks like the perfect trade. We did, after all, hit max profit.

However, it’s extremely difficult to hold short options to expiration. Beyond the emotional rollercoaster, you’ve also got to worry about assignment risk, especially with American-style options like IBIT.

Let’s take a look under the hood of this trade and see what actually happened:

IBIT Strangle: Trade Explanation

What grabbed my attention immediately was that huge spike in the value of our put with around 7DTE, where it was trading just under $6. With only 7 DTE, assignment risk here was very high. Remember, assignment risk increases when:

- An option's intrinsic value is high

- Expiration approaches

Additionally, in the days leading up expiration, gamma risk spikes. This is because small changes in the underlying price can cause large changes in delta, making positions harder to hedge and more sensitive to movement.

I find exiting strangles (and straddles) before one week to expiration helps avoid these risks and locks in gains while extrinsic value remains. When extrinsic value is gone, there’s no incentive to hold the options because their value is tethered to the stock price.

IBIT: Losing Trade Outcome

37 days have passed, and expiration is upon us. Although the trade started off nicely, staying within the range of our strikes and eating away at the value of our options, IBIT screamed higher in the last 10 days of trading. Here’s where we ended:

- IBIT Price: $59.64 → $75.00 ⬆️

- Expiration: 37 days → 0

- Sell 65 Call @ $1.53 → $10.00

- Sell 55 Put @ $1.31 → $0.00

- Final Value: $10.00 (call closed deep in the money)

- Net Loss: $2.84 – $10.00 = –$7.16 (–$716 total)

- Percent of Max Profit: 0% ❌

- Percent Lost vs Max Profit: –252%

Let’s go to the chart now to see how this played out in real time:

Right off the bat, I can see that the short call option was likely to be assigned around 3 DTE, which would have forced us to sell the stock at $65/share. This is because IBIT uses American-style options like all stocks and ETFs. It’s one of the reasons I prefer to trade European-style options on indexes like SPX, NDX, and VIX — there’s virtually no assignment risk.

Looking a little closer at the chart, we can see that this strangle was trading around $1.40 with 21 days to expiration. That represents about half of our total profit potential. I would have exited the trade here, or maybe even before.

Choosing Deltas on Short Strangles

In options trading, delta is the option Greek that tells us how much an option's value may change given a $1 move up or down in the underlying asset. Delta also tells us:

- The number of shares an option ‘trades like’

- The probability an option has of expiring in the money

Let’s focus on the second bullet here. A true neutral short strangle involves selling out of the money options. We want to sell options with a low probability of landing in the money at expiration. Standard deviations can help with strangle strike selection.

Let’s explore this relationship more now:

Standard Deviation and Corresponding Deltas

Here’s what 1, 2, and 3 standard deviations mean in terms of probability and delta in options trading:

We’re selling the 16 delta call and the 16 delta put, so the combined delta is around 32. That means there’s roughly a 32% chance one of these options expires in the money, which implies a 68% chance they both expire out of the money, which is obviously what we want.

You can sell lower delta options if you want a higher probability of success. But the trade-off is clear: you won’t collect much premium, and you’ll likely have to sell a higher quantity of strangles to make it worthwhile.

That’s what I like to call picking up pennies in front of a steamroller.

Selecting Deltas: TLT Trade Example

Here’s an example of the 1 SD deltas I like on the TradingBlock dashboard for TLT (iShares 20+ Year Treasury Bond ETF). The net delta here is .33 (thirty-three as we say), giving this trade a 67% chance of success.

Short Strangles and Time Decay (Theta)

Short options benefit from time decay, which is the predominant reason most professional traders sell options rather than buy them.

With the passage of time, assuming all else stays the same, like price and IV, options contracts lose value. This time decay really starts to speed up as expiration gets closer, accelerating noticeably around 45 days to expiration (DTE).

.png)

Therefore, options sellers may want to choose expiration dates at or near this 45 DTE mark. When you sell options like LEAPs with a long time until expiration, you'll be waiting a while for time decay to pick up while tying up a lot of cash in margin, which could otherwise earn a nice return at the risk-free rate.

Theta is the option Greek that represents how much value an option is expecting to shed with every passing day.

Reminder: Aim to exit strangles at least one week before expiration. Most extrinsic value is gone by this time, and gamma risk picks up. Price movements get sharper, more volatile, and less forgiving. There’s less premium left to gain and much more to lose.

Short Strangles and Implied Volatility

You want to sell strangles when implied volatility is relatively high and expected to come down. Remember, IV is like a tide that lifts all option prices, calls and puts alike. Many traders like to sell strangles before major events like earnings or economic releases (e.g., the jobs report) in hopes that IV will collapse afterward. This is known as an IV crush, and option sellers love it.

So, how do you know if IV is relatively high?

- Check IV rank or IV percentile. These tell you where current IV stands compared to its past. Higher numbers = richer premiums.

- Compare implied vs. historical volatility. If IV is much higher than recent realized volatility, the market may be overpricing future movement.

Professional traders more widely use the former because it directly reflects how expensive options are relative to their history.

Managing Short Strangle Risks

Short strangles require active management, particularly if you’re trading American-style options, which are subject to early assignment. Here are a few things to watch for:

1. Monitor Breakout Moves

If the stock starts creeping toward either strike, especially with 14 days or less to expiration, be on alert to manage. Gamma picks up, risk accelerates, and rolling or closing becomes a smart move, not a reactive one.

2. Know When to Take Profits

Don't wait around for every last penny. If you're sitting on 50% of your max profit with half the time left, take the win. The market doesn’t reward greed.

3. Watch for Volatility Shifts

A sharp drop in implied volatility is your best friend when you’re a net seller of options. But if IV starts climbing after you’ve entered the trade, your position could quickly turn against you. Manage accordingly.

4. Check Liquidity

Whenever placing an options trade, always use a limit order. If you want to get filled quickly, place your order at the mid-point, which is between the bid and ask price. Work your strangle down in penny or nickel increments if you don’t get filled right away.

Also, make sure to run through the main liquidity metrics and look for any red flags, such as:

- Wide bid/ask spreads

- Low open interest

- Low volume

If you're trading illiquid strikes, you will likely have issues getting filled at a decent price, particularly when volatility jumps. Learn more about options liquidity here.

Long Straddle vs Short Straddle

The short strangle is a neutral options trade. You’re betting the stock stays between two strikes and that volatility stays in check. The long strangle is, therefore, the opposite of this trade:

- Short strangle: Sell an out of the money call and an out of the money put. Limited reward, significant risk, but high probability of profit if the stock stays put.

- Long strangle: Buy an out of the money call and put. Low probability, high reward: you're hoping for a big move in either direction.

Short Straddle vs Short Strangle

.png)

The short straddle and strangle have a lot in common. In short, if you have strong conviction about where the stock will land, sell a straddle. If you want more breathing room, sell a strangle. The wider your strangle strikes, the more leeway you have, but the less premium you’ll collect.

Short Strangles and The Greeks

In options trading, the Greeks are a series of risk tools that hint at the future price of an option based on changes in different variables. Here are the 5 most important Greeks to know:

- Delta – Measures how much the option price moves relative to the underlying stock.

- Gamma – Tracks how Delta changes as the stock moves.

- Theta – Measures time decay, showing how much value the option loses daily.

- Vega – Sensitivity to implied volatility, affecting option price.

- Rho – Measures impact of interest rate changes on the option price.

And here is the relationship between short strangles and these Greeks:

⚠️ Short strangles are advanced, high-risk trades. They carry unlimited loss potential on the call side and substantial downside risk on the put side. This strategy is not suitable for all investors. Trade outcomes can be significantly impacted by assignment risk, commissions, fees, and slippage—none of which are reflected in the examples above. Always read The Characteristics and Risks of Standardized Options before trading.

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

FAQ

Both are neutral, long volatility trades. A straddle buys the call and put at the same strike, while a strangle uses different strikes, making it cheaper, but requires a bigger move to win.

The short strangle involves selling two naked options, so it is a very risky strategy. However, it's less risky than selling a single naked option because of the premium you collect from both the call and the put. Only one side can expire in the money.

The short strangle is a high probability trade, but by no means is it always profitable. The further out of the money the options you sell, the higher your likelihood of success, but the less premium you collect.

The maximum loss on a short strangle is theoretically infinite because the strategy involves selling a call option naked. Losses can be substantial if the stock makes a large move in either direction.

The short straddle is better if you forecast very little movement and want maximum premium. The short strangle is better if you expect some movement but not too much and want more breathing room.

Short strangles benefit from the natural time decay in options and from a drop in implied volatility. They also give you flexibility based on how far out you set your strikes.