VXX vs VIX Options: Key Differences for Traders

In this article, we break down the key differences between VXX and VIX options, including how each product is structured, how they settle, where risk hides, and which is better suited for short-term trading versus longer-term hedging.

.png)

iPath Series B S&P 500 VIX Short-Term Futures ETN (VXX) and the CBOE Volatility Index (VIX) are both volatility-tracking products that offer options trading, but that is where their similarities end. Their structural differences drive meaningfully different behavior, settlement mechanics, and risk profiles, especially for options traders.

Highlights

- VIX measures expected volatility, not market direction, which is why volatility products can move independently of stocks, sometimes rising or falling alongside the market.

- VXX does not track the VIX index, as it gains exposure through short-term VIX futures, introducing roll costs and structural decay over time.

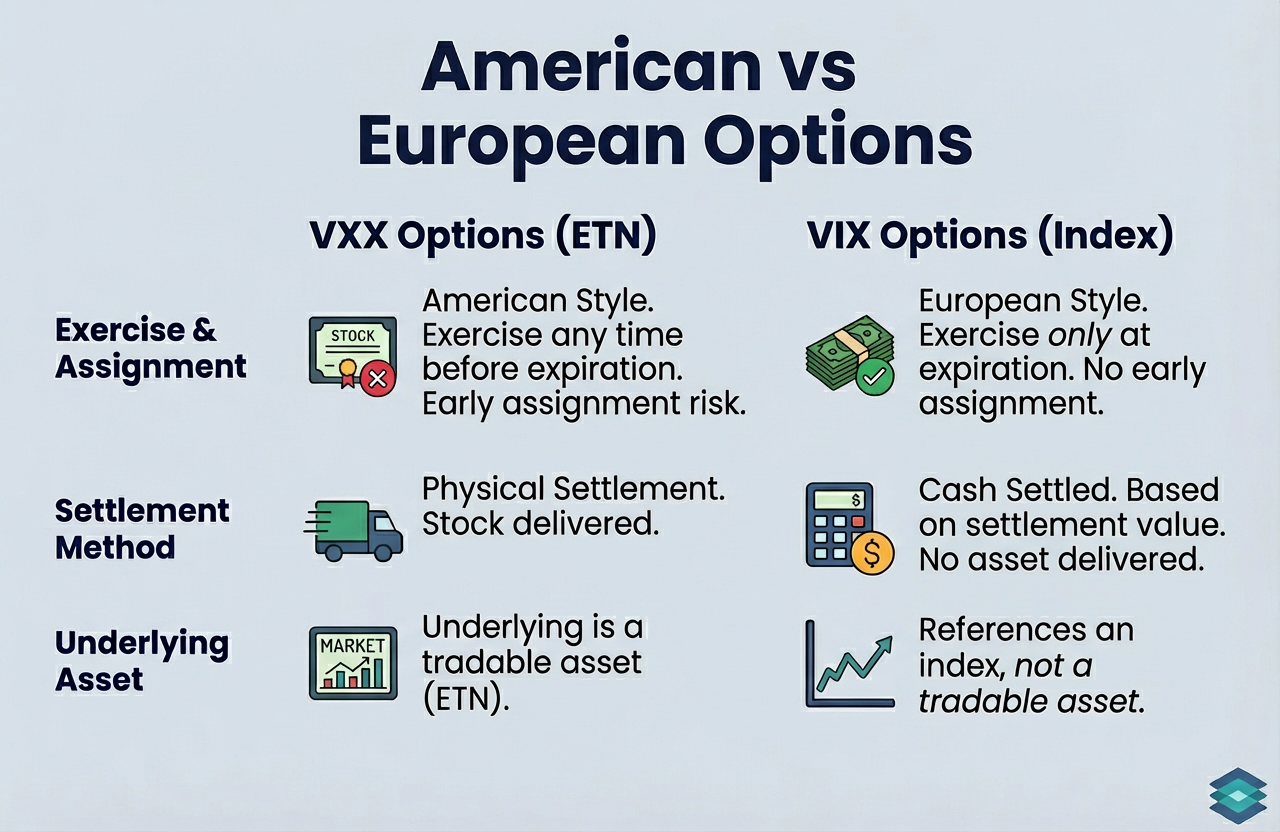

- VXX options are American style, meaning they can be exercised early and assigned into a stock position, adding assignment and stock risk.

- VIX options are European style and cash settled, eliminating early assignment risk and avoiding any underlying delivery at expiration.

- Volatility products are tactical tools, not investments, best suited for short-term speculation or defined hedging windows rather than long-term holding.

What is VIX?

VIX is the ticker symbol for the CBOE Volatility Index, often referred to as the market’s “fear gauge.” It measures the market’s expected volatility over the next 30 days, derived from the premiums of near-term S&P 500 index options.

Key points that matter:

- VIX is not futures-based.

- It is calculated directly from option prices, not from VIX futures.

- Because of that, VIX itself does not decay the way futures-based products do.

- It reflects implied volatility, not past price movement.

An elevated VIX signals that traders are paying up for protection, implying larger expected price swings in the near term.

What is VXX?

VXX is an exchange-traded note (ETN) issued by Barclays Bank PLC. Unlike ETFs, ETNs are unsecured debt instruments backed by the issuer’s credit.

Structurally:

- VXX holds front-month and second-month VIX futures

- Those futures expire

- The position must be continually rolled

VXX: Buyer Beware!

That rolling is the problem.

Most of the time, VIX futures trade in contango (longer-dated futures priced higher than near-term futures). As VXX rolls:

- It sells cheaper expiring futures

- Buys more expensive longer-dated futures

The difference creates structural value decay over time.

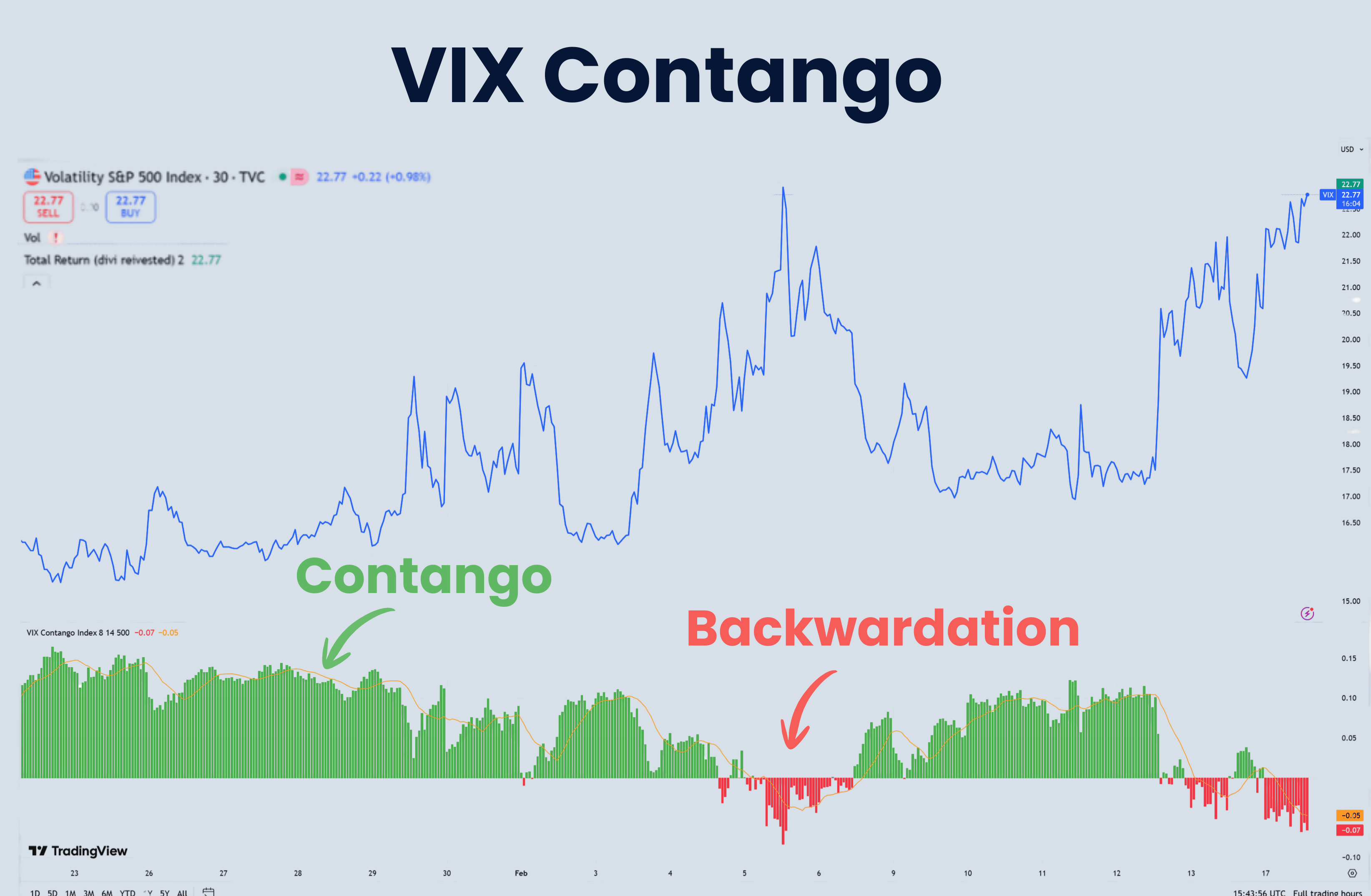

We can see in the TradingView chart above that, in high-volatility environments, VIX sometimes trades in backwardation, but this is rare. Backwardation implies that near-term VIX futures are priced above longer-dated contracts. For VXX, this temporarily reduces or even reverses its usual roll decay. But this environment is rare.

Let’s now take a look at VXX’s decay in action and compare it to VIX on a 5-year chart:

.png)

As we can see, VXX lost ~66 percentage points more than VIX, or about 3.6× the drawdown of the VIX over the same period.

To sum the VXX ETN up:

- It is not suitable for long-term holding

- Even holding longer than a few days increases exposure to roll decay

- It is best used for very short-term tactical trades

So we just learned the difference between VIX and VXX. Before we get more granular, let’s explore why these products exist in the first place, and if they may be helpful to you!

Why Trade Volatility Products?

Volatility products can be used to:

- Hedge portfolios against market drawdowns. A long volatility position can help cushion equity losses during sudden selloffs.

- Speculate on rising or falling volatility. Traders may buy VIX call options ahead of events like CPI releases or Fed meetings, or sell options when implied volatility appears overpriced.

- Gauge market stress and near-term risk. Rising volatility levels often reflect increasing fear.

Most professional traders and money managers monitor VIX constantly (even if they never trade it) because it provides a real-time read on expected near-term price movement. When the VIX is up, prices are moving.

VXX vs VIX: Liquidity

Both VXX and VIX offer strong options liquidity, with typically tight markets and high volume and open interest. That liquidity is usually concentrated in near-dated options (front week or front month) and thins out as option expirations extend further into the future and LEAPS.

For VIX options specifically, liquidity is deepest in the standard monthly expirations, while weekly options can be noticeably thinner.

American vs European Style Options

There are two main types of option contracts: American style and European style. Here’s what they each imply.

American-style options (VXX)

Most stocks and exchange-traded products, including VXX, use American-style options.

These options:

- Can be exercised and assigned at any time prior to expiration

- Subject to early assignment risk

- Settle via physical delivery

- Assignment results in a stock position in VXX

VXX Assignment Example

Let’s take a look at a sample assignment on a short call position in VXX:

- You are short the VXX 29 strike price call

- VXX is trading at 30

- The option holder exercises early

- You are assigned and must sell 100 shares at 29

- If you do not own shares, you become short 100 shares of VXX

European-style options (VIX)

Index options such as the CBOE Volatility Index (VIX) are European style. This means:

- No early exercise: eliminates early assignment risk

- Cash settled: based on how far the option finishes in the money at settlement

- Underlying: references an index level, not a tradable asset

VXX options behave like equity options tied to a tradable product, while VIX options avoid early exercise and settle cleanly in cash.

VIX Assignment Example:

Let’s take a look at a sample assignment on a short put position in VIX:

- You are short the VIX 22 put

- VIX settles at 21 at expiration

- The option finishes 1 point in the money

- VIX options are European style, so there is no early assignment

- The option cash settles at expiration

- You owe 1 point × $100 = $100 per contract

- No shares are delivered

AM vs PM Option Settlement

VIX and VXX settle at different times of the day. Settlement timing affects how and when option values are finalized at expiration, which can meaningfully impact outcomes.

VIX options (AM settlement)

VIX options settle in the morning on expiration day using the special opening quotation (VRO). This means the final value is determined by the opening prices of the constituent options, not where VIX trades intraday. As a result, outcomes can differ meaningfully from the prior close. This can shock many traders and make positions difficult to hedge!

VXX options (PM settlement)

VXX options settle the typical way at market close on expiration day. Because VXX is a tradable exchange-traded product, the option’s value is based on the closing price of VXX, which generally aligns more closely with what traders see during the session.

VIX vs VXX: Which is Best?

If you want to trade the underlying product directly, VXX is the most commonly used exchange-traded vehicle for expressing short-term long volatility exposure, largely due to its liquidity and accessibility.

However, if your goal is to sell volatility, shorting VXX outright introduces two key risks:

- Cost to carry the short stock position

- Unlimited upside risk during volatility spikes

Because of this, many traders instead use ProShares Short VIX Short-Term Futures ETF (SVXY), which provides inverse volatility exposure without the mechanics of short stock.

Best for Options

Generally speaking, VXX is favored for short-term options speculation because it is liquid, equity-style, and easy to trade tactically, even though its structure embeds persistent decay. 0DTE options are particularly popular because, like equity options, these options settle at the market close.

For medium- to longer-term hedging, I prefer VIX options. This avoids the ongoing roll decay embedded in VXX, eliminates early assignment risk through European-style settlement, and avoids the challenge of hedging with a product that exists in a near-perpetual state of decay.

Risks of Volatility Trading

Volatility products are typically reserved for experienced traders. They behave very differently from stocks and ETFs, and are not a starting point for most options traders.

Here are four key risks to know:

- Volatility is not the market - VIX measures expected volatility, not market direction

- Timing matters more than direction - being “right” on fear is not enough

- Decay works in the background - many volatility products lose value over time

- Short-term tools, not investments - designed for tactical use, not buy-and-hold

Summary Table

Let’s conclude the article with a summary table of everything we have learned!

⚠️ Trading VIX and VXX options involves substantial risk and is not suitable for all investors. Examples in this article are for educational purposes only and do not include commissions or fees, which can significantly affect trade outcomes. Always review The Characteristics and Risks of Standardized Options before trading and ensure you understand how each product works before committing capital.

FAQ

The VIX tells you how much volatility the market is pricing in over the next 30 days based on S&P 500 option premiums.

A historically low VIX implies little fear in the market and is typically associated with neutral to bullish conditions, while a high VIX signals elevated uncertainty and demand for protection.

VIX is an index derived from option prices that measures expected volatility, while VXX is a tradable ETN that gains exposure through short-term VIX futures.

VXX tracks VIX futures rather than the VIX index itself, and rolling those futures over time introduces decay that causes performance to diverge.

VXX options are American-style options on the VXX ETN that settle into shares and can be exercised or assigned prior to expiration.

.png)

.png)