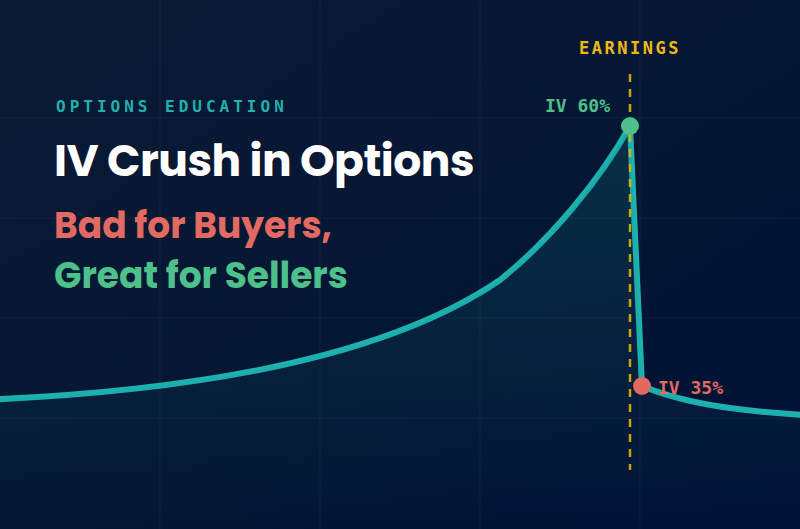

IV Crush in Options: Bad for Buyers, Great for Sellers

You bought a call. The company beat earnings. The stock gapped higher. Your call still lost money. That is IV crush, and it catches option buyers almost every earnings season.

Options carry a premium for uncertainty, and the moment earnings hit the tape, that uncertainty is gone and so is the premium. That is why a long call can bleed on a good report while the trader who sold it can turn a profit.

Highlights

- IV crush is the sharp drop in implied volatility once a scheduled event passes. Earnings are the classic trigger, and the option loses extrinsic value even if the stock barely moves.

- Buyers have to beat the expected move, not just the direction. Options are priced for the event before it happens.

- Sellers can collect the inflated premium, but the credit is capped and the losses are not.

- Some traders buy the ramp and sell before the report. It's a vega-versus-theta race, and the ramp is never guaranteed.

What Is IV Crush?

Implied volatility crush, usually shortened to IV crush, is a sharp drop in an option's implied volatility after a scheduled event passes. An earnings announcement is the classic case. The uncertainty gets resolved, the market no longer needs to price in a big move, and the volatility component of every option on that name deflates at once.

The mechanics matter here. An option's price has two parts: intrinsic value and extrinsic value. Intrinsic value is what the option is worth if exercised at the current price. In other words, it is how much an option is in the money by. Extrinsic value is everything else, and it runs on two inputs:

- Time. It drains out of an option on a schedule you can see coming. This is called theta: options shed value with each passing day, assuming no change in price or IV.

- Implied volatility. It can change in a single session, which makes it the swing factor in an option's price.

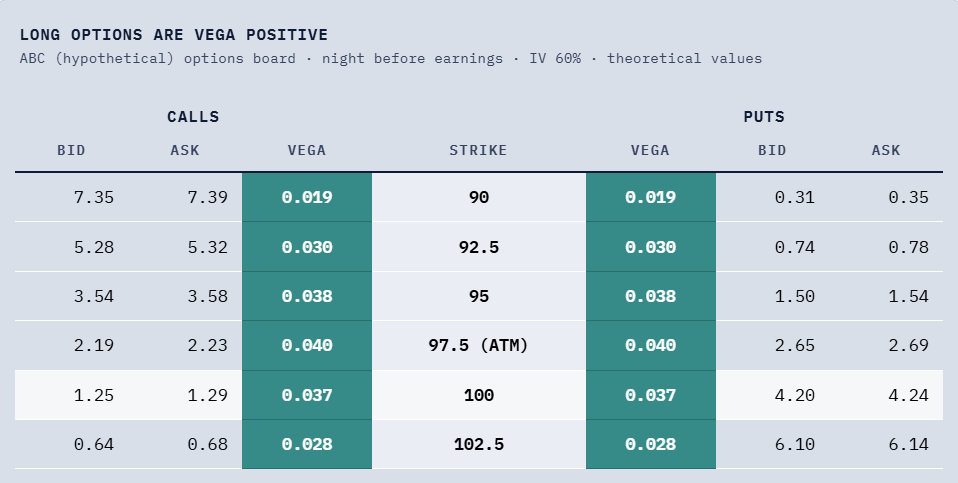

Implied volatility is the options market's estimate of future volatility in the underlying asset. More expected movement means more premium. When IV collapses, extrinsic value collapses with it. Vega measures exactly this exposure: how much an option's price changes per point of implied volatility. The stock does not have to move a single penny for the crush to hit.

Calls and puts alike lose value when IV falls, and vega peaks at the money. $0.04 per point sounds small until IV drops 25 points overnight: roughly $1.00 of extrinsic value gone per share, no stock move required.

Vega peaks at the money. An at the money option is the closest thing to a coin flip, so nearly all of its value is extrinsic. Change the expected move and those contracts reprice the most.

Deep in the money options act more like stock, and far out of the money options are cheap either way. Both care less when IV moves. The crush hits hardest right where most earnings traders buy.

Why Implied Volatility Spikes Before Earnings

Market makers are not going to sell you cheap options into a known binary event. As an earnings report approaches, market uncertainty rises, and demand for protection and speculation pushes option prices up. Higher option prices mean higher implied volatility. It is the same relationship read in both directions. Elevated volatility is just the options market charging more premium for event risk. Broad market volatility can lift IV across every name at once, but the pre-earnings ramp is specific to the stock reporting.

The pattern is remarkably consistent: IV grinds higher for two to three weeks into the report, peaks the day of, then collapses the moment the number is out. The chart below shows the market's expectation building and then unwinding on our fictional stock.

The Buyer's Side: Right on Direction, Wrong on the Trade

Numbers make this concrete. ABC, our fictional name, trades at $97 with earnings tonight and the weekly expiration date four days out. Implied volatility on the front weekly is 60%, up from the mid 30s where it normally sits. You buy the call at the 100 strike price for $1.27.

The report is good. ABC beats. The stock opens the next morning at $99, up about 2%. Implied volatility collapses from 60% to 35%. Here is your position:

The stock moved 2% in your favor and the call still dropped 34%. The actual price changes helped you. The volatility repricing buried you. Break the overnight change apart and the 2% rally added about $0.78 at unchanged volatility. One day of time decay took back $0.33. The IV crush took another $0.88, the biggest line item of the night and more than the rally added after decay.

The Expected Move: What the Market Already Priced In

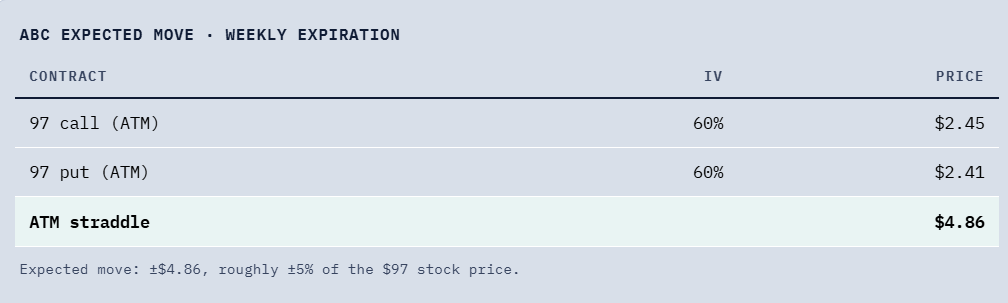

Here is the part most new option buyers skip. Before the event, the options board tells you how big a move the market expects. The quickest read is the at-the-money straddle in the expiration that captures the event. Add the call and the put at the same strike and you have the number.

That is the real bet a pre-earnings option buyer is making. It is not "will the stock go up." It is "will the actual move beat what the options board already priced in." Calling the expected direction is not enough, and neither is beating earnings estimates. Getting just the direction right buys you nothing if the option cost too much. The stock has to beat the expected move. When the stock moves less than the options imply, sellers tend to come out ahead. When it moves more, buyers do.

The Seller's Side: Getting Paid for the Crush

Flip the trade and everything that hurt the buyer becomes the seller's opportunity. Option sellers collect that inflated extrinsic value and can profit when IV collapses and the stock stays inside the expected move. Selling premium into the event means selling options at a higher price and aiming to buy them back at lower prices after the crush. It is how experienced options traders potentially capitalize on the same event that punishes buyers.

Same fictional setup. Instead of buying the call, a trader sells the ABC 92/102 strangle: short the 92 put and short the 102 call, collecting $1.41 total. Both strikes sit just outside the expected move.

Be clear about what this trade is before going further. A short strangle carries substantial risk. The credit is capped at $141 per contract. The loss is not. If ABC gaps far enough through either strike, the damage can run to several times the credit collected, and the short call side has no ceiling at all.

ABC opens at $99 the next morning with IV at 35%. Both options deflate hard. The strangle that sold for $1.41 can be bought back for about $0.31. That is roughly $1.10 of profit per share, or about $110 per contract, in one session. The seller did not need to predict the direction. They needed the move to stay inside the expected range, and they needed the crush. In this example, they got both.

The Catch, Because There Is Always a Catch

Selling options into earnings is not free money. Traders who sell options here are getting paid to take on tail risk. Run the same trade and let ABC gap to $107 instead. The short 102 call goes deep in the money and the strangle costs about $5.20 to buy back. That is a loss of roughly $3.79 per share, or $379 per contract, well over triple the maximum profit. Naked short options carry substantial risk, and a short call has unlimited risk on paper.

This is why the expected move keeps both sides honest. Options are priced for roughly a 5% swing because sometimes the stock actually delivers a 10% one. Large price swings are exactly the risk the seller takes on. IV crush is a real, recurring market dynamic, but selling into it means collecting a limited credit while accepting the possibility of much larger losses. Whether that trade-off fits comes down to account size and risk tolerance. Many compare selling options to picking up pennies in front of a steamroller: you might make 15 successful grabs in a row, but the 16th can wipe out years of profits. Position accordingly.

Beyond Earnings: Where Else IV Crush Shows Up

Earnings get the headlines, but major events with a known date and an unknown outcome can inflate options and set up a crush:

- FDA decisions and clinical trial readouts. Biotech is the extreme case. IV on small drug developers can reach triple digits ahead of a binary approval decision, then drop sharply the morning after.

- Merger and acquisition news. Deal speculation inflates IV. A confirmed deal at a fixed price can crush it almost to zero, since the stock is now pinned to the buyout terms.

- Macro events. Fed decisions, CPI prints, and jobs reports do the same thing to index options. SPY options expiring just after a Fed meeting might carry 17% IV, pricing roughly a 1% move by the end of the week, while the surrounding expirations sit several points lower. Once the statement drops, that premium bleeds out the same way it does in a single stock. A hypothetical: with SPY at $630 and a Fed decision the day before Friday expiration, the ATM straddle might trade near $6.33 at 17% IV. The next morning, with the decision out and IV back near 12%, that same straddle is worth about $3.16. Roughly $1.30 of that drop is a day of theta. The rest is the crush. The VIX, which tracks 30-day implied volatility on the S&P 500, has historically averaged near 20 and tends to sag after major scheduled events pass without surprises.

- Legal rulings and political outcomes. Court decisions, regulatory votes, elections. Resolution is the trigger, not the result. IV can crush on bad news just as hard as on good news.

When IV Crush Is Bad for You

- You bought options before the event. Long calls and puts can lose value when implied volatility collapses after a company's earnings report.

- The stock move falls short of expectations. Even being directionally correct may not be enough if the move is smaller than the options market priced in.

- You paid a high volatility premium. The more inflated IV was before the announcement, the more option premium can disappear once the uncertainty is gone.

When IV Crush Works for You

- Short premium into the event. Short strangles, straddles, and iron condors are all structured to collect premiums while IV is inflated and aim to buy them back cheaper after the crush. Defined risk structures like the iron condor cap the tail scenario in exchange for a smaller credit.

- Spreads instead of single legs, even when you are directional. A debit spread like a bull call spread pairs a long option with a short one at a higher strike. The short leg gets crushed too, which offsets most of the vega damage. You give up some upside to stop paying the volatility tax.

- Owning options when IV is cheap. The mirror image of the whole article. Long premium tends to work best when implied volatility is low relative to its own history, not the night before a binary event.

Buy the Rumor, Sell Before the News

There is a third way to trade the event: own options during the ramp and get out before the report. Buy premium while IV is still low, ride the run-up, and sell before the number is out. You collect the inflation and skip the crush. None of this is guaranteed.

It is a race between vega and theta, and it can easily lose. In the front weekly, theta usually wins even when the ramp shows up: a 100 call bought three weeks out for $2.53 can be worth about $1.27 by report day with the stock flat. A 45-day call fares better in the same hypothetical, roughly $4.07 to $4.38, because longer dated options carry more vega and bleed less theta. But if IV rises late, stays flat, or never ramps at all, that $4.07 call can drift to about $3.07. This is a bet on the market's anticipation, and anticipation can no-show.

How to Check Before You Trade

Three numbers every options trader should check before routing the order, all available on the options board:

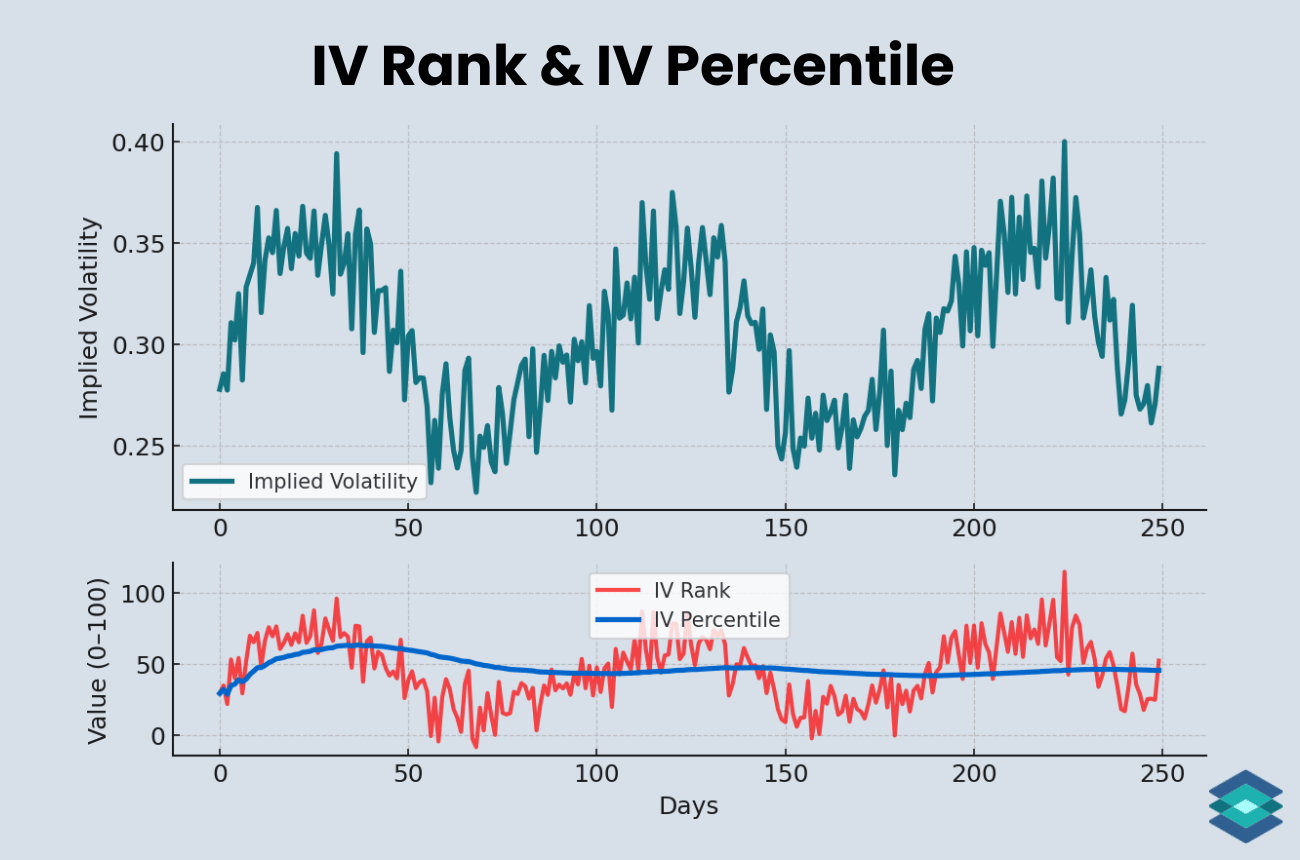

- IV rank or IV percentile. Where does current IV sit against the past year? A 60% IV means nothing in isolation. If a stock's IV has ranged between 30% and 65% over the past 52 weeks and now sits at 60%, its IV rank is about 86. That tells you the market is pricing something unusual and you are buying near the top of the range. Volatility has historically tended to revert toward its average, which is why traders watch these extremes.

- The expected move. Price the ATM straddle in the expiration that captures the event. That is the hurdle. If you do not believe the stock beats it, buying premium is a hard way to make the point.

- The stock's actual history. Compare the implied earnings move to the stock's actual price movements over its last eight reports. When options consistently imply 5% and the stock consistently moves 2%, that gap has historically favored the sellers on that name. Past patterns can break, but you should at least know what they were.

None of this makes IV crush avoidable. It is a structural feature of how options price events. But it is visible in advance. The traders who get hurt by it are usually the ones who never checked.

FAQ

IV crush happens the moment scheduled uncertainty gets resolved, usually right after the company reports earnings. Most earnings releases land after hours, so the crush shows up at the next open. IV typically drops within the first minutes of trading.

No. Implied volatility drops sharply even if the underlying stock opens flat. The crush hits whether or not the underlying asset moves, because the event premium comes out of the option either way.

Yes, but far less. Longer dated options spread the event premium across more time, so when IV falls after the report, the same drop takes a smaller percentage bite.

No. Theta is the slow daily cost of holding an option. IV crush is a rapid decline in the volatility priced into the option, and it can happen in a single session. Theta is rent. The crush is a repricing.

.png)