Naked Calls and Puts: A Guide to Selling Options

Naked options are high-probability, high-risk credit trades. You collect premium up front, but if the market turns against you, the losses can be brutal. Here's everything you need to know about selling options naked.

Selling options naked means collecting premium in exchange for taking on real risk. Naked calls carry unlimited loss potential, and naked puts can hand you a substantial loss if the stock collapses. Traders sell them anyway, for the income, the high probability of success, and the edge that comes with elevated implied volatility.

Highlights

- Naked means uncovered. You sell a call or put without owning the stock or hedging it, collecting premium up front in exchange for taking on the obligation that comes with being short.

- Naked calls have unlimited loss potential but a moderately high success rate relatively to other options strategies.

- Naked puts carry defined but very high risk, with that same moderately high success rate working in your favor.

- Time decay, or theta, works in your favor when shorting options because as each day passes with no change in price and IV, the option you sold loses a little value.

- Bull put and bear call spreads cap your risk by pairing the option you sell with a further-OTM long.

What Are Naked Options?

Just as with stocks, you can both buy and sell options.

- When you buy an option to open a position, you are said to be "going long."

- When you sell an option to open a position, you are said to be "going short," or, as we often say in the industry, going naked.

Being naked also implies you have no long options hedging your exposure. You have a lot of risk, which is why it is called being naked - you’re fully exposed. To better understand this risk, let's first look at how a short stock position works.

Suppose you short 100 shares of ABC stock at $100 per share. The most you can make is $100 per share, which happens if the stock falls to zero. Your risk, however, is theoretically unlimited because there is no cap on how high a stock can rise.

A naked call option has a similar risk profile. The difference is that options are leveraged instruments, meaning a relatively small move in the stock can result in a much larger gain or loss. Because of this leverage, naked options are generally considered among the riskiest options strategies.

In this article, we’ll tell you everything you need to know about selling options naked; the pros, cons, risks involved, and a few alternative strategies that may allow you to sleep at night.

Long vs. Short (Naked) Options

When you buy an option, you go long. You pay a premium for the right to either buy stock at the strike (long call) or sell stock at the strike (long put). Your risk is capped at what you paid for the option. Your upside can be big.

.png)

When you sell an option naked, you go short. You flip the whole thing around. You collect the premium up front, but now you carry the obligation.

- Long option: Limited risk, large potential reward, lower probability of profit.

- Short (naked) option: Limited reward, large potential risk, higher probability of profit

By obligation, we are referring to assignment risk. When/if a long call holder decides to exercise their option, you must deliver 100 shares to them, netting your account -100 shares. For puts, it's the reverse: when the long put holder exercises, you're obligated to buy 100 shares at the strike, netting your account +100 shares (and the cash to pay for them out of your account).

This physical delivery of shares is reserved for equity and ETF options, which are called American-style options. European-style options, like SPX options, settle in cash instead.

Most traders start out buying options because the risk is easy to understand. You can only lose what you paid. When you sell options naked, you collect small, steady premiums and bet that the big move most buyers are hoping for never shows up.

Why Traders Sell Naked Options

Traders sell options naked for two reasons: time and volatility work for you, not against you. (For a broader look, see our guide on selling options for income.)

- Income. You collect premium up front. If the option expires worthless, that credit is yours to keep.

- High probability of success. Out-of-the-money options expire worthless more often than not. Sell far enough out of the money and the odds are on your side.

- Time decay (theta). With the passage of time, all else equal, the option you sold loses value. As the seller, that decay is money in your pocket.

- Elevated implied volatility. When IV is high, premiums are fat. Sell rich premium, and if volatility falls, the option deflates and you can buy it back cheap.

But high IV is a double-edged sword. You're collecting more premium for a reason. The market is telling you it expects a significant move ahead. You get paid more because you're taking on more risk.

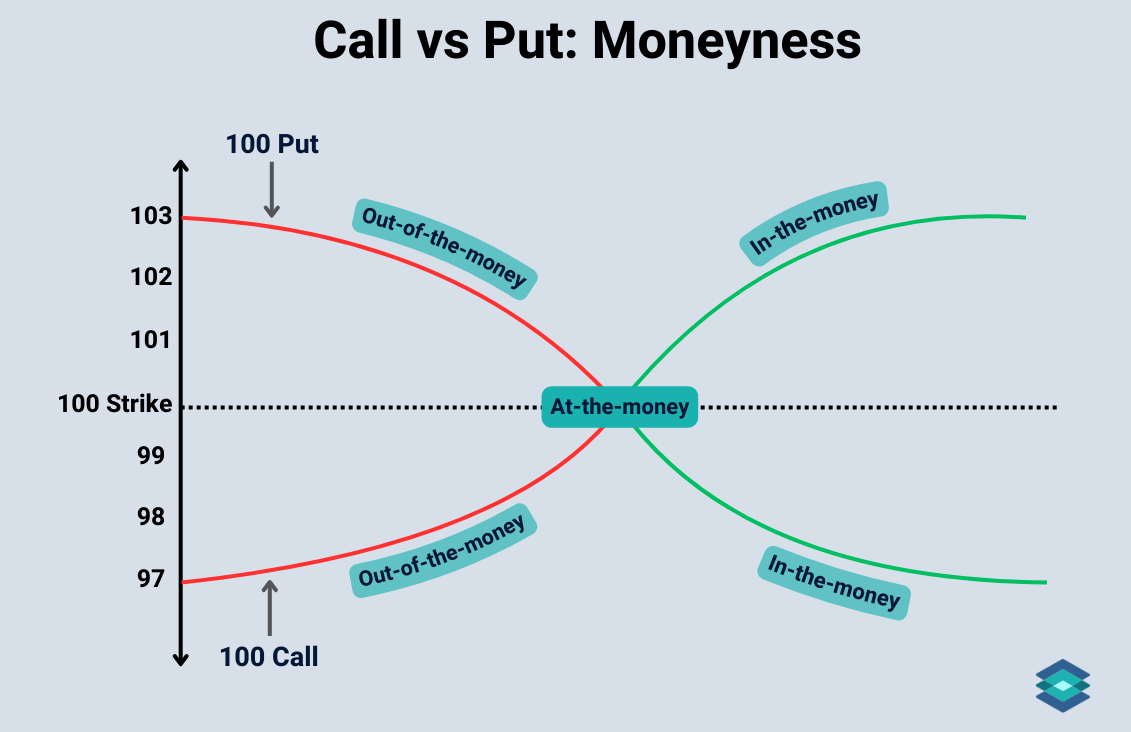

Moneyness and Choosing a Strike

Once you've decided to sell premium, the next question is which strike. That comes down to moneyness, the relationship between the strike price and where the underlying is trading.

When you sell naked, you almost always want to sell out-of-the-money. A call is OTM when the strike sits above the current price; a put is OTM when the strike sits below it. OTM options carry no intrinsic value, only extrinsic value, and that extrinsic value is exactly what decays in your favor as time passes.

How far out of the money is the trade-off. Sell closer to the money and you collect a fatter premium, but your probability of success drops and assignment risk climbs. Sell further out and the premium thins, but the odds the option expires worthless tilt in your favor.

Naked Calls Explained

A naked (short) call is an undefined-risk, high-probability, market-neutral to bearish trade with unlimited loss potential. You sell a call without owning the underlying, collecting premium and betting the stock stays below your strike through expiration.

Naked short calls are the sirens of the options trading world. Their high probability of success and steady income generation lure traders with a high-risk appetite. But in the long run, most traders get humbled. One bad day can wipe out months or years of profit. And when the market turns against you, it tends to turn fast.

The best time to sell a naked call is when you're neutral to bearish on the underlying and implied volatility is elevated. But you don't want to be too bearish, your max profit is capped at the premium collected.

The Risk is Real

This is why professional traders often compare selling options naked to picking up pennies in front of a steamroller. The risk is substantial, especially with call options, where the potential loss is infinite since there's no cap on how high a stock can go.

A friend of mine traded on the CBOE years ago, making a killing selling naked calls on a high-beta tech stock. Then came the acquisition announcement. The stock exploded, and his floor trading days were over before lunch.

Naked Call Payoff Profile

Selling a call has limited upside and unlimited risk. Here's how the payoffs break down:

Max Profit: The premium you collect. Sell the 95 strike price call on ABC for $0.75 ($75) with the stock at $90, and as long as ABC closes below $95 at expiration, you keep the full $75.

Max Loss: Unlimited. There's no cap on how high a stock can go. If ABC gets acquired and rips to $135, that call is now $40 in the money. You've lost $4,000, minus the $75 you collected, for a net loss of $3,925. All to make $75.

Breakeven = Strike + Premium → $95 + $0.75 = $95.75.

Naked Call Example

Let's sell an out-of-the-money call on SPY (the SPDR S&P 500 ETF Trust), expiring in 39 days, targeting a strike about 5% out of the money on the SPY options chain. We chose SPY for its broad market exposure, high liquidity, and deep selection of strikes and expirations.

SPY is trading at $730 today. We will sell the 765 strike call, expiring in 39 days, for a credit of $2.85 ($285):

- Position: Short 1 SPY Call

- Premium Collected: $2.85 ($285)

- Expiration: 39 days

- Strike: $765

- Current Price: $730

- Breakeven: $767.85

- Margin Requirement: ~$11,200

We sold this call for $2.85, meaning we'll pocket the full $285 if SPY stays below $765 on option expiration. Our breakeven is $767.85. Anything above that, and we're in the red. Bear in mind the high margin requirement for that trade.

Short Call Trade Outcomes

39 days have passed, and expiration is upon us. Let’s look at two difference trade outcomes.

Positive Outcome

Markets cooled off and SPY drifted to $740, safely below our strike. The call expired worthless, we kept the full $285, and the margin was released.

Negative Outcome

A blowout jobs report sent SPY ripping to $785, well above our strike. The call we sold for $2.85 is now worth $20, a loss of $1,715 ($20 − $2.85, times 100). That's the risk with naked uncovered calls: limited reward, unlimited downside. In the real world, this one likely gets assigned a day or two early, since it's deep in the money with almost no extrinsic value left.

Naked Puts Explained

A naked (short) put is a high-probability, market-neutral to bullish trade with substantial downside risk if the stock collapses. It's a net credit trade best used when implied volatility is elevated. You sell a put, collect premium, and bet the stock stays above your strike through expiration.

I used to fill orders for a customer who stuck to one trade: selling puts on stocks he liked. Like a lot of traders, he liked the idea of "getting paid to wait" for a stock to drop to a price he was willing to buy at. If he liked ABC at $45 but it traded at $50, he'd sell the 45-strike put, keep the premium, and roll out until he got assigned and happily bought the shares.

But over time, he drifted away from the cash-secured approach and began selling puts without sufficient funds to cover assignment. He'd sell the option and forget about it. That worked fine… until it didn't. When the 2008 financial crisis hit, his account was liquidated. I never heard from him again.

Naked Put Example

Let's sell a ~4% out-of-the-money put on SPY (the SPDR S&P 500 ETF Trust), expiring in 44 days. Same reasoning as before: broad exposure, high liquidity, deep strike selection.

I chose the $705 strike because the premium was fat ($6.47), theta was a healthy $0.16/day, and IV was elevated at around 17%, which boosts premium and gives us an edge as sellers.

- Position: Short 1 SPY Put

- Premium Collected: $6.47 ($647)

- Expiration: 44 days

- Strike: $705

- Current Price: $730

- Breakeven: $698.53

- Margin Requirement: ~$10,400

Short Put Trade Outcomes

44 days have passed, and expiration is upon us. Let's look at two different trade outcomes.

Positive Outcome

Markets were bearish but SPY held above our strike the whole time, closing at $712. The put expired worthless and we kept the entire $647.

Negative Outcome

Markets sold off hard and SPY closed at $685, putting our put deep in the money. At expiration it's worth its intrinsic value of $20. Since we collected $6.47, our loss is $20 − $6.47 = $13.53 per share, or $1,353 total, well past our max profit of $647. In the real world this one likely gets assigned before expiration, since the deeper in the money it goes and the closer expiration gets, the higher the early-assignment risk.

Margin Requirements for Naked Options

Selling options naked comes with extremely high margin requirements. Since you're taking on theoretically unlimited (calls) or substantial (puts) risk, your broker has to protect itself if the trade moves against you.

The requirement is typically based on the higher of two calculations, multiplied by the number of contracts and the standard 100 multiplier:

- 20% of the underlying price, minus the out-of-the-money amount, plus the premium

- 10% of the underlying price (calls) or strike price (puts), plus the premium

Using the ABC short call example (stock $90, strike $95, premium $0.75):

- Formula 1: (20% × $90) − $5 OTM + $0.75 = $13.75/share → $1,375 per contract

- Formula 2: (10% × $90) + $0.75 = $9.75/share → $975 per contract

Brokers use the higher number, so the requirement here is $1,375 per contract. Also keep in mind margin requirements vary widely by broker.

Risks of Naked Options

The risks with selling options naked are real. Here are a few to keep in mind.

1. Catastrophic loss potential. Naked calls carry unlimited risk. There's no ceiling on a stock. Naked puts carry substantial risk down to zero. Either way, your max loss dwarfs your max gain.

2. Assignment risk. In-the-money options are always at risk of being assigned. That risk goes up the deeper in the money they are, and the closer expiration gets. Get assigned and you're suddenly long or short 100 shares per contract.

3. Implied volatility risk. A spike in IV can push your short option's price higher even if the stock goes nowhere. IV tends to spike fast, and at the worst possible time.

4. Margin calls. If the market turns against you fast and you don't have enough cash to meet a call, your account can be liquidated. In my experience, this happens at the worst possible time, with the worst possible fills. Keep extra cash on hand.

5. Dividend risk (calls). If your short call is in the money near the ex-dividend date, the call buyer will likely exercise early to collect the dividend. That leaves you short the stock and on the hook for paying it.

6. Opportunity cost. Naked options tie up enormous margin. If you sell a LEAPS call for $1 and it ties up $2,000 in margin for a year, wouldn't it make more sense to park that money in Treasuries and earn a similar return, without taking on unlimited risk?

Naked Options vs. Spreads

The single most effective way to tame naked-option risk is to turn it into a vertical spread, buying a further out-of-the-money option against the one you sell. You give up some premium, but you cap your max loss at a number you decide. I love selling options, but I've got a weak stomach when it comes to risk.

That's exactly why spreads like the bear call are some of my favorite trades: they profit from time decay while keeping the maximum risk defined at the level I choose.

Bear Call Spread, The defined-risk version of a naked call. Sell a call, buy another further OTM call, same expiration. Net credit, neutral-to-bearish, profits when the stock stays below the short strike. Example: sell a 6300/6310 call spread on SPX for $1.00 net credit, risking $9.00 to make $1.00, with the loss capped at the spread width.

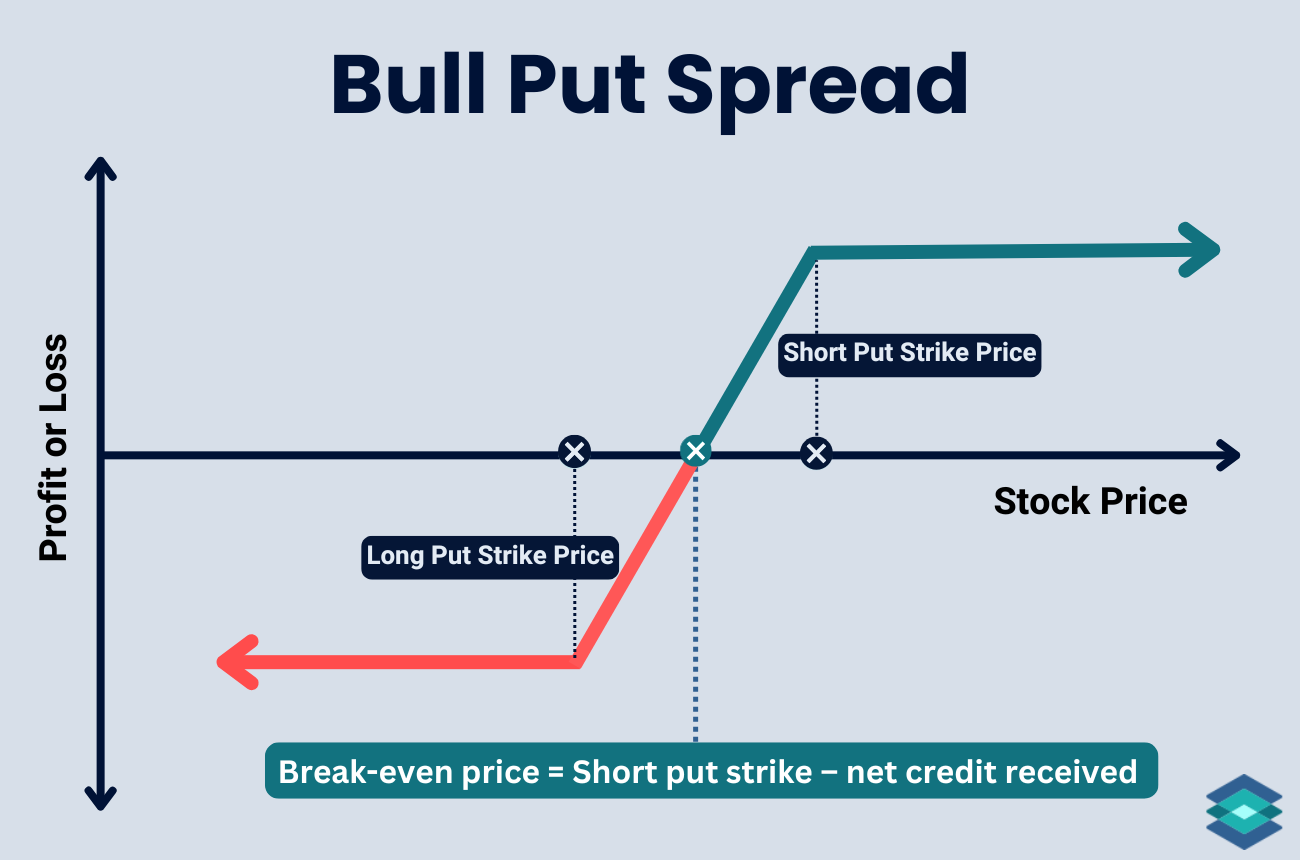

Bull Put Spread, The defined-risk version of a naked put. Sell a put, buy another further OTM put, same expiration. Net credit, neutral-to-bullish, profits when the stock stays above the short strike. Example: sell a 6250/6240 put spread on SPX for $0.55 net credit, risking $9.45 to make $0.55, with the loss capped at the spread width.

Selling 0DTE Naked Options

Selling naked options is a high-probability but high-risk way to trade 0DTE (zero days to expiration) options. It is a straightforward method of taking advantage of time decay, but is best reserved for seasoned traders. You don't want to learn by selling options naked on expiration day, I assure you.

Most traders prefer trading European-style 0DTE options (SPX, NDX, and VIX) because European-style options are cash settled, meaning you don't have to deliver the actual underlying shares if and when you're assigned.

They're also exercisable only at expiration, so you don't carry the early-assignment risk that comes with American-style equity and ETF options. For a naked seller, that's one less thing that can blow up your position before the close.

Naked Options and The Greeks

Before entering a naked short trade, it's essential to understand the Greeks. Start with delta, it gives you a rough idea of the probability your option expires in the money. Use that number to weigh the risk against the premium you're collecting. Is the trade worth it? Remember, for a short call, the risk is infinite.

Once the trade is on, shift your focus to gamma. With 0DTE, gamma risk is extreme. A small move in the underlying can flip your position fast. What looks safe in the morning can be deep in the money by the close.

When to Use Naked Calls and Naked Puts

It comes down to two simple questions: How directional am I, and how fast do I think the move (or lack of one) plays out?

Sell a naked call when:

- You're neutral to slightly bearish on the underlying.

- Implied volatility is elevated (you're being paid for the risk).

- You're not expecting a big decline, if you were, a long put or bear put spread rewards you more.

- You can stomach unlimited risk, or you cap it with a bear call spread.

Sell a naked put when:

- You're neutral to slightly bullish.

- IV is elevated, ideally high and expected to fall.

- You're ok with the risky, you'd genuinely be happy owning the stock at the strike (cash-secured), or you've capped the risk with a bull put spread.

For both: time decay starts to accelerate around 45 days to expiration, which is a solid window to target. Choose strikes further OTM for higher probability and less premium; closer to the money for more premium and more assignment risk.

Managing Naked Options

Naked options aren't passive, the position you put on at 30 delta can be sitting at 60 next week. If a trade moves against you, roll it out in time (calendar spread) for more premium, or roll up or down (vertical spread)to a new strike. However, if you've captured most of your max profit, buy it back and walk away. Don't get greedy over pennies.

FAQ

A naked call option is when you sell a call on an underlying asset without hedging it with stock or other options. It’s a high-risk trade with unlimited loss potential if the stock takes off.

Generally speaking, brokers require investors to have some experience with trading options and get approved before they can sell options naked. Selling options naked is typically the highest level, or level 3.

Short puts are at risk of assignment when expiration approaches and/or the option has significant intrinsic value, meaning the stock price is below the strike price. If assigned, you'll be obligated to buy the underlying stock at the strike price.

The most common way to exit a short put is by buying it back with a limit order before expiration. If you hold it through expiration and it closes in the money, you may be assigned and required to buy the stock at the strike price.

You should sell a put option when you are neutral to bullish on an underlying asset. Out-of-the-money short puts are best for neutral to bullish markets, while in-the-money short puts are suitable when you're more confident the stock will not drop below the strike price.

.png)

.png)

.png)